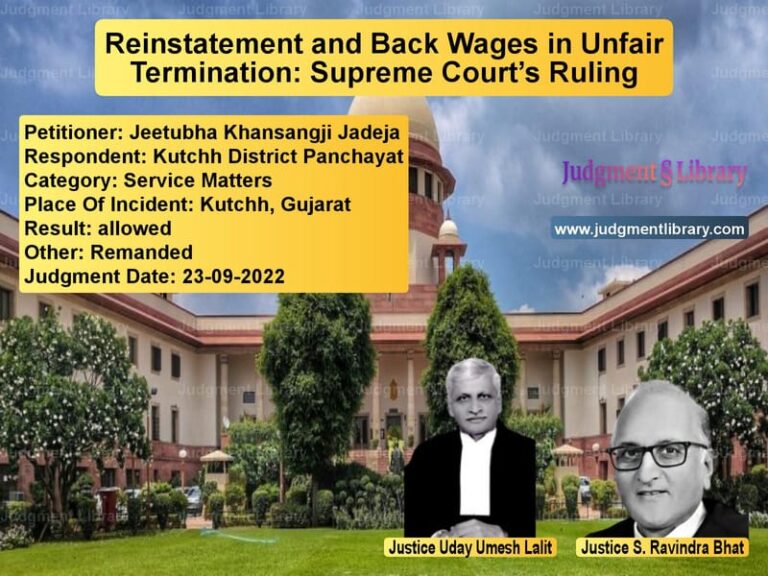

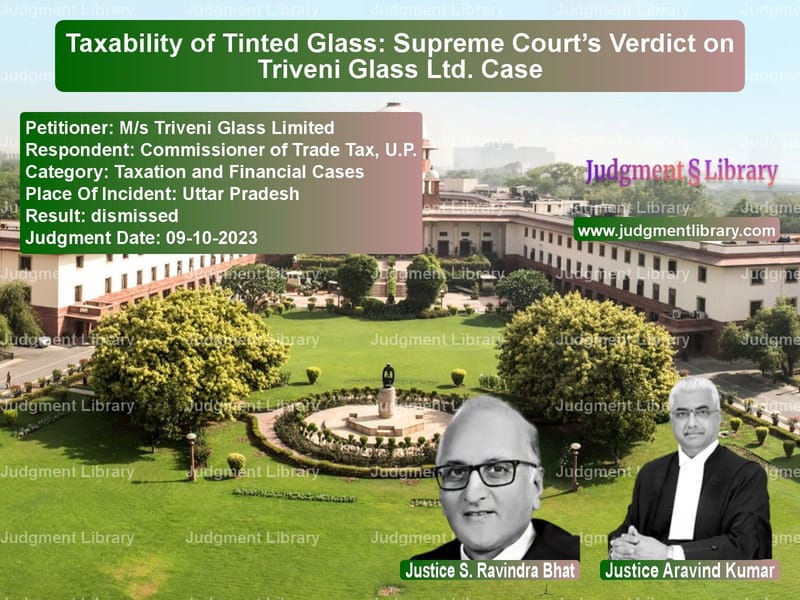

Taxability of Tinted Glass: Supreme Court’s Verdict on Triveni Glass Ltd. Case

The Supreme Court of India recently ruled on a long-standing dispute regarding the taxability of tinted glass sheets manufactured by M/s Triveni Glass Ltd. The case revolved around whether tinted glass should be classified under the category of ‘goods or wares made of glass’ and thus be subjected to a higher tax rate or be treated as an unclassified item with a lower tax rate. This decision holds significance for businesses dealing in glass products and tax authorities alike.

Background of the Case

The appeals originated from tax assessment disputes spanning multiple years, including 1996-97, 1992-93 to 1996-97, 1998-99, and 2003-04. M/s Triveni Glass Ltd., a company engaged in the manufacturing of various types of glass, contended that tinted glass was fundamentally the same as plain sheet glass and should be taxed at a lower rate. However, tax authorities held that tinted glass was a distinct product and fell under the category of ‘all goods and wares made of glass,’ attracting a higher tax rate of 15% under Notification No.5784 dated 07.09.1981.

Petitioner’s Arguments

Shri S.K. Bagaria, appearing for Triveni Glass Ltd., argued that:

- Tinted glass is merely colored sheet glass and does not undergo any fundamental transformation that would classify it differently from plain glass.

- The difference in color does not alter the nature or function of the glass, and thus, tinted glass should be taxed at the same rate as plain sheet glass.

- The manufacturing process for tinted and plain glass is essentially the same, apart from the addition of certain coloring agents.

- Previous tax assessments had categorized tinted glass as plain glass, and the change in classification was unwarranted.

Respondent’s Arguments

Shri R.K. Raizada, representing the tax authorities, countered that:

- The manufacturing process of tinted glass differs from that of plain glass, involving additional raw materials like cobalt oxide, carbon oxide, and iron oxide.

- Tinted glass has distinct characteristics such as different transparency levels and higher solar radiation absorption.

- The product is not commercially recognized as plain sheet glass in the market.

- Previous assessments were erroneous, and the revised classification correctly reflected the nature of the product.

Findings of the High Court

The High Court dismissed the petitioner’s claims, ruling that tinted glass cannot be equated with plain sheet glass. The court observed that tinted glass was manufactured in a separate unit, had different density and transparency, and was distinctly recognized in commercial trade. The court upheld the tax authorities’ classification, affirming that tinted glass fell within the category of ‘goods and wares made of glass.’

Supreme Court’s Verdict

Justice Aravind Kumar, delivering the Supreme Court’s judgment, upheld the High Court’s decision. The ruling emphasized:

- The phrase “all goods and wares made of glass” in Notification No.5784 was broad enough to include tinted glass.

- The exclusion of “plain glass panes” from the notification indicated that only uncolored, ordinary glass was exempt from the higher tax category.

- Market perception plays a critical role in determining tax classifications. In commercial parlance, tinted glass was not considered equivalent to plain sheet glass.

- Judgments from previous cases, including Atul Glass Industries (Pvt.) Ltd. vs. Collector of Central Excise and Geep Flashlight Industries Ltd. vs. Union of India, were cited to support the principle that tax classification should align with how a product is understood in trade.

Conclusion

The Supreme Court’s decision establishes a crucial precedent for determining the taxability of specialized glass products. The ruling reinforces that commercial perception, manufacturing process, and product characteristics are key determinants in tax classification. Businesses dealing in tinted glass and similar products must now account for the higher tax rate, aligning their compliance strategies accordingly.

Petitioner Name: M/s Triveni Glass Limited.Respondent Name: Commissioner of Trade Tax, U.P..Judgment By: Justice S. Ravindra Bhat, Justice Aravind Kumar.Place Of Incident: Uttar Pradesh.Judgment Date: 09-10-2023.

Don’t miss out on the full details! Download the complete judgment in PDF format below and gain valuable insights instantly!

Download Judgment: ms-triveni-glass-li-vs-commissioner-of-trad-supreme-court-of-india-judgment-dated-09-10-2023.pdf

Directly Download Judgment: Directly download this Judgment

See all petitions in Income Tax Disputes

See all petitions in Tax Refund Disputes

See all petitions in Customs and Excise

See all petitions in Judgment by S Ravindra Bhat

See all petitions in Judgment by Aravind Kumar

See all petitions in dismissed

See all petitions in supreme court of India judgments October 2023

See all petitions in 2023 judgments

See all posts in Taxation and Financial Cases Category

See all allowed petitions in Taxation and Financial Cases Category

See all Dismissed petitions in Taxation and Financial Cases Category

See all partially allowed petitions in Taxation and Financial Cases Category