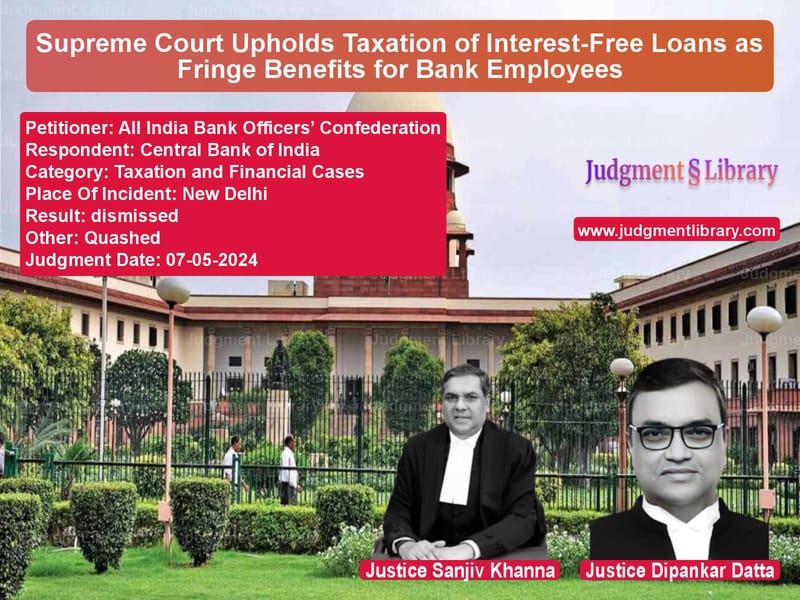

Supreme Court Upholds Taxation of Interest-Free Loans as Fringe Benefits for Bank Employees

The case of All India Bank Officers’ Confederation vs. The Regional Manager, Central Bank of India & Ors. deals with the legality of taxing interest-free and concessional loans provided to employees of banks as ‘fringe benefits’ under the Income Tax Act, 1961. The petitioners challenged the provisions under Section 17(2)(viii) and Rule 3(7)(i) of the Income Tax Rules, arguing that they were unconstitutional and unfairly applied to loans provided to bank employees. The Supreme Court dismissed the appeals, upholding the taxability of these loans as perquisites.

Background of the Case

The petitioners, representing various bank officers and unions, challenged the constitutional validity of Section 17(2)(viii) of the Income Tax Act and Rule 3(7)(i) of the Income Tax Rules, which include interest-free and concessional loans provided by banks to their employees as taxable perquisites. These provisions deem the benefit of the concessional loan as a ‘fringe benefit’, making it liable for taxation. The petitioners argued that such taxation was arbitrary and violated their constitutional rights.

Chronology of Events

- 2014: The appeal was filed by the All India Bank Officers’ Confederation and other petitioners challenging the vires of Section 17(2)(viii) and Rule 3(7)(i) of the Income Tax Rules, 1961.

- 2015: The petitioners argued that the application of these provisions for taxing interest-free loans was excessive and amounted to an unconstitutional delegation of legislative powers.

- 2017: The Delhi High Court dismissed the petitioners’ appeal, ruling that the rules were constitutionally valid.

- 2024: The Supreme Court, after hearing the appeals, upheld the High Court’s judgment, reinforcing the legality of the provisions and dismissing the challenge.

Legal Issues Considered

The Supreme Court considered several important legal questions:

- Whether Section 17(2)(viii) and Rule 3(7)(i) of the Income Tax Rules, 1961, which tax interest-free loans as perquisites, amount to excessive delegation of legislative functions.

- Whether the classification of interest-free loans as fringe benefits is arbitrary and violative of Article 14 of the Constitution of India, which guarantees equality before the law.

- Whether the rule-making authority’s decision to set the interest rate benchmark to the Prime Lending Rate (PLR) of the State Bank of India (SBI) was arbitrary.

Arguments by the Appellants (All India Bank Officers’ Confederation)

The petitioners, represented by Senior Advocate Rajiv Dutta, argued that:

- The provisions of Section 17(2)(viii) and Rule 3(7)(i) amount to an unconstitutional delegation of legislative powers to the Central Board of Direct Taxes (CBDT), as it allows the CBDT to prescribe fringe benefits that can be taxed.

- The taxation of interest-free loans as perquisites is arbitrary and violates the principle of equality under Article 14 of the Constitution.

- The fixing of the SBI Prime Lending Rate (PLR) as the benchmark for determining the value of concessional loans is unjust, as it does not reflect the actual interest rates charged by banks.

Arguments by the Respondents (Central Bank of India and Others)

The respondents, represented by Senior Advocate Abhishek Manu Singhvi, contended that:

- Section 17(2)(viii) and Rule 3(7)(i) are valid legislative provisions that have been implemented to ensure fairness in the taxation of fringe benefits.

- The taxation of interest-free loans as perquisites ensures that all benefits received by employees are treated uniformly and fairly under the Income Tax Act.

- The use of SBI’s PLR as the benchmark is not arbitrary, as SBI’s interest rates reflect the market conditions and are used as a standard by other banks.

Supreme Court’s Judgment

The Supreme Court ruled in favor of the respondents, upholding the constitutional validity of Section 17(2)(viii) and Rule 3(7)(i) of the Income Tax Rules. The Court held:

“The provisions of Section 17(2)(viii) and Rule 3(7)(i) are within the permissible scope of delegated legislation. They do not amount to excessive delegation of essential legislative functions. The classification of interest-free loans as fringe benefits is a valid exercise of the legislative power, and the use of the SBI’s PLR as the benchmark is not arbitrary or unconstitutional.”

- The Court held that the delegation of power to the CBDT was not excessive, as it was specifically constrained by the language of Section 17(2)(viii), which provided clear guidelines for what constitutes a perquisite.

- The Court also emphasized that tax laws related to fringe benefits enjoy greater flexibility and that a single benchmark for calculating perquisites is reasonable and practical for ensuring consistency and clarity in taxation.

- The Court dismissed the petitioners’ claim of arbitrariness in the taxation of interest-free loans, stating that such benefits fall squarely within the definition of perquisites under the law.

Impact of the Judgment

The judgment has significant implications for taxation policies and employee benefits:

- Clarity on Taxation of Fringe Benefits: The ruling clarifies the legal status of interest-free loans and other similar fringe benefits as taxable perquisites under the Income Tax Act.

- Strengthening the Legislative Framework: The Court upheld the delegation of powers to the CBDT to prescribe the value of fringe benefits, ensuring that the regulatory authority can effectively manage tax laws.

- Precedent for Employee Benefits Taxation: The decision sets a precedent for the treatment of other similar employee benefits and reinforces the principle that such benefits are taxable when provided by an employer.

Conclusion

The Supreme Court’s decision in All India Bank Officers’ Confederation vs. The Regional Manager, Central Bank of India affirms the constitutionality of taxing interest-free loans and other fringe benefits as perquisites under the Income Tax Act, 1961. By upholding the power of the CBDT to prescribe what constitutes a fringe benefit, the Court ensures a fair and consistent application of tax laws. The ruling provides clarity on the taxation of employee benefits and reinforces the flexibility of tax measures in commercial settings.

Petitioner Name: All India Bank Officers’ Confederation.Respondent Name: Central Bank of India.Judgment By: Justice Sanjiv Khanna, Justice Dipankar Datta.Place Of Incident: New Delhi.Judgment Date: 07-05-2024.

Don’t miss out on the full details! Download the complete judgment in PDF format below and gain valuable insights instantly!

Download Judgment: all-india-bank-offic-vs-central-bank-of-indi-supreme-court-of-india-judgment-dated-07-05-2024.pdf

Directly Download Judgment: Directly download this Judgment

See all petitions in Income Tax Disputes

See all petitions in Banking Regulations

See all petitions in Judgment by Sanjiv Khanna

See all petitions in Judgment by Dipankar Datta

See all petitions in dismissed

See all petitions in Quashed

See all petitions in supreme court of India judgments May 2024

See all petitions in 2024 judgments

See all posts in Taxation and Financial Cases Category

See all allowed petitions in Taxation and Financial Cases Category

See all Dismissed petitions in Taxation and Financial Cases Category

See all partially allowed petitions in Taxation and Financial Cases Category