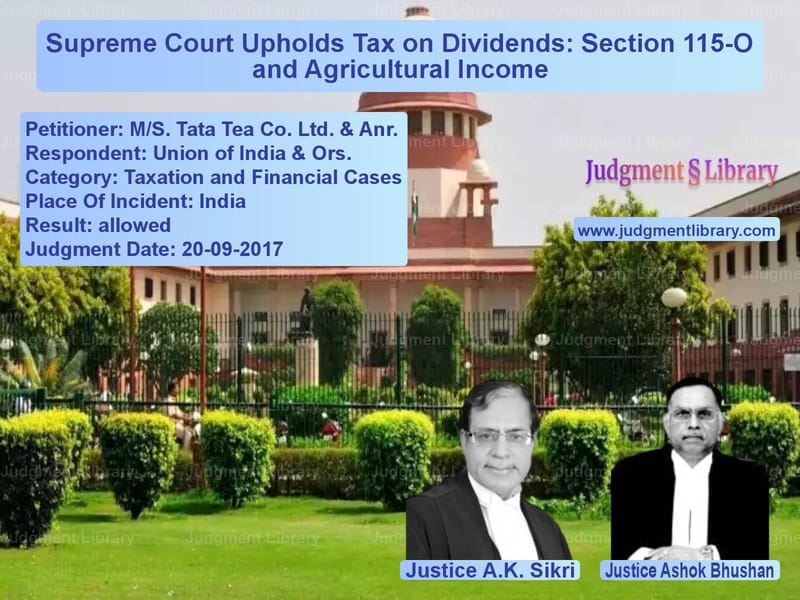

Supreme Court Upholds Tax on Dividends: Section 115-O and Agricultural Income

The Supreme Court of India recently delivered a significant judgment in Union of India & Ors. v. M/S. Tata Tea Co. Ltd. & Anr. and related appeals, concerning the constitutional validity of Section 115-O of the Income Tax Act, 1961. This provision, introduced by the Finance Act of 1997, imposes an additional tax on dividends distributed by domestic companies. The primary contention in this case was whether this tax encroached upon agricultural income, which falls exclusively under state jurisdiction.

The case involved multiple appeals arising from judgments of the Calcutta High Court and the Gauhati High Court. The petitioners, comprising prominent tea companies such as Tata Tea Ltd., George Williamson (Assam) Ltd., and Apeejay Surrendra Corporate Services Ltd., challenged the imposition of tax under Section 115-O, arguing that it indirectly taxed their agricultural income, which is beyond the legislative competence of Parliament under the Constitution of India.

Background and Legal Context

Section 115-O of the Income Tax Act was introduced to levy an additional income tax on domestic companies distributing dividends to their shareholders. The key provision states:

“Notwithstanding anything contained in any other provision of this Act and subject to the provisions of this section, in addition to the income tax chargeable in respect of the total income of a domestic company for any assessment year, any amount declared, distributed, or paid by such company by way of dividends shall be charged to additional income tax.”

The petitioners argued that a substantial portion (60%) of their income was agricultural income derived from tea cultivation, which is constitutionally exempt from Union taxation under Entry 46 of List II of the Seventh Schedule. They contended that taxing dividends sourced from this income amounted to an unconstitutional levy.

Arguments by the Petitioners

The tea companies advanced the following key arguments:

- Tax on Agricultural Income: The petitioners contended that 60% of their income derived from growing tea was agricultural income, which under Rule 8 of the Income Tax Rules, 1962, is exempt from taxation by the Union.

- Lack of Legislative Competence: The petitioners argued that under the Constitution, Parliament cannot impose taxes on agricultural income, and by subjecting dividends to additional tax under Section 115-O, it effectively extended its taxation powers beyond its jurisdiction.

- Double Taxation: It was argued that since corporate tax was already paid on the taxable portion (40%) of their income, imposing an additional tax on dividends amounted to double taxation.

- Judicial Precedents: The petitioners relied on past rulings, including Mrs. Bacha F. Guzdar v. Commissioner of Income Tax, to argue that agricultural income remains protected even when distributed as dividends.

Counterarguments by the Union of India

The Union of India, defending the constitutionality of Section 115-O, submitted the following counterarguments:

- Change in the Character of Income: Once a company declares a dividend, the nature of the income changes from business/agricultural income to dividend income, which can be taxed separately.

- Legislative Competence: Parliament has the exclusive power to tax all incomes other than agricultural income under Entry 82 of List I. The tax under Section 115-O is on dividend distribution, not agricultural income.

- Precedent from Supreme Court Judgments: The government relied on past rulings that held dividends to be distinct from the source of profits and, therefore, taxable at the hands of the company.

Supreme Court’s Analysis

The Supreme Court carefully examined the constitutional framework, including Article 246, which distributes legislative powers between the Union and the States. The Court applied the doctrine of pith and substance to determine whether Section 115-O encroached upon the State List.

The Court also referred to judicial precedents such as Prafulla Kumar Mukherjee v. Bank of Commerce, Khulna, which emphasized that a law must be examined in its true nature and substance rather than incidental encroachments.

The Court held:

- Dividends lose their agricultural character: The Court reaffirmed the principle that when a company distributes dividends, they cease to be agricultural income and take on a new form as shareholder earnings.

- Entry 82 (Taxes on Income) is broad: The Court ruled that Section 115-O falls squarely under Entry 82, which allows taxation of all incomes except agricultural income. The additional tax is imposed on dividend distribution, not on the agricultural process itself.

- No interference with State List: The Supreme Court disagreed with the Calcutta High Court’s limitation that only 40% of dividend income could be taxed, stating that such an interpretation modifies the statute in a way not intended by the legislature.

Judgment and Conclusion

The Supreme Court upheld the validity of Section 115-O and allowed the Union of India’s appeals, setting aside the restrictive ruling of the Calcutta High Court. The appeal by the petitioners was dismissed.

The Court concluded:

“Dividend income, once declared and distributed, is no longer agricultural income. The imposition of additional tax under Section 115-O is constitutionally valid and does not violate the division of legislative powers.”

The ruling establishes an important precedent in taxation jurisprudence, affirming that once profits are distributed as dividends, they can be taxed under Union legislation, regardless of their original nature. This decision has far-reaching implications for companies with agricultural income streams and clarifies the taxability of dividends under Indian law.

Don’t miss out on the full details! Download the complete judgment in PDF format below and gain valuable insights instantly!

Download Judgment: MS. Tata Tea Co. Lt vs Union of India & Ors Supreme Court of India Judgment Dated 20-09-2017.pdf

Direct Downlaod Judgment: Direct downlaod this Judgment

See all petitions in Income Tax Disputes

See all petitions in Tax Evasion Cases

See all petitions in Tax Refund Disputes

See all petitions in Judgment by A.K. Sikri

See all petitions in Judgment by Ashok Bhushan

See all petitions in allowed

See all petitions in supreme court of India judgments September 2017

See all petitions in 2017 judgments

See all posts in Taxation and Financial Cases Category

See all allowed petitions in Taxation and Financial Cases Category

See all Dismissed petitions in Taxation and Financial Cases Category

See all partially allowed petitions in Taxation and Financial Cases Category