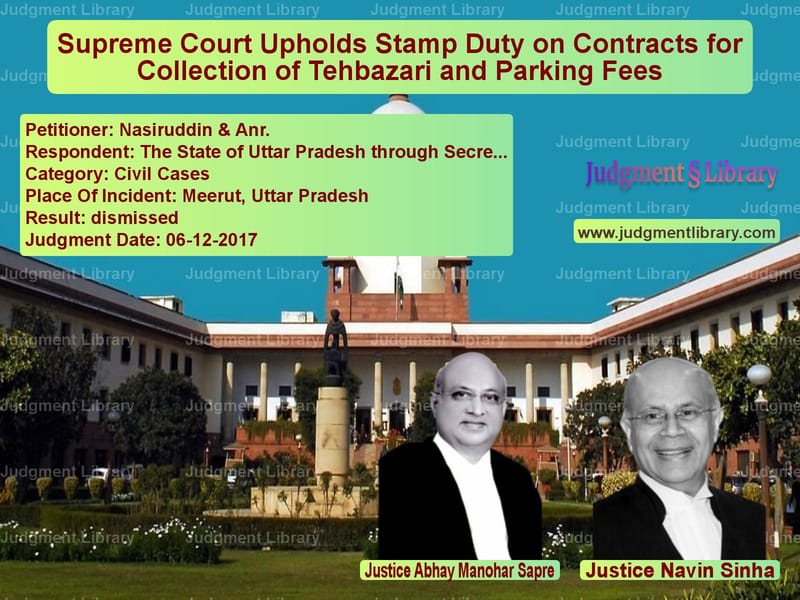

Supreme Court Upholds Stamp Duty on Contracts for Collection of Tehbazari and Parking Fees

The Supreme Court of India, in the case of Nasiruddin & Anr. vs. The State of Uttar Pradesh & Ors., delivered a significant judgment on the applicability of stamp duty on contracts awarded for collecting Tehbazari (vendor fees) and parking fees by municipal corporations. The Court upheld the decision of the Allahabad High Court, affirming that such contracts should be treated as leases under the Indian Stamp Act, 1899 and charged accordingly.

This ruling clarifies the nature of municipal contracts for toll collection and their legal treatment under stamp duty laws, ensuring that the government does not suffer revenue losses due to incorrect classification of such agreements.

Background of the Case

The case involved multiple appeals challenging the demand for stamp duty imposed by the Collector of Stamps on contracts awarded by the Nagar Nigam Meerut (Municipal Corporation Meerut) and other municipal bodies in Uttar Pradesh. The municipal corporations had invited bids for granting rights to collect:

- Tehbazari Fees: Charges levied on squatters, vendors, and kiosk owners for occupying public spaces.

- Parking Fees: Charges collected from vehicle owners for parking in designated areas.

The appellants, who had won these contracts, were directed to pay stamp duty at the rate of Rs. 70 per thousand on the contract amount, treating these agreements as leases under the Indian Stamp Act, 1899. They challenged this demand in the Allahabad High Court, which dismissed their petitions, leading to the present appeals before the Supreme Court.

Petitioners’ (Contractors’) Arguments

The appellants contended that:

- The contracts were licenses, not leases, and should not attract lease stamp duty.

- The contracts did not grant any interest in immovable property but merely authorized them to collect fees on behalf of the municipality.

- As per New Bus-Stand Shop Owners Association vs. Corporation of Kozhikode (2009), similar agreements were treated as licenses.

- The demand for higher stamp duty was excessive and arbitrary.

State’s Counterarguments

The State of Uttar Pradesh argued that:

- The agreements fell within the definition of “lease” under Section 2(16)(c) of the Indian Stamp Act, 1899, as they involved the letting of toll collection rights.

- The contractors were granted exclusive rights to collect fees, making these agreements more than mere licenses.

- The Allahabad High Court had already ruled on similar matters, upholding the lease classification.

- Any loss of revenue due to misclassification of agreements would affect municipal governance.

Supreme Court’s Observations

The Supreme Court, in a judgment delivered by Justice Abhay Manohar Sapre and Justice Navin Sinha, made the following key observations:

“The expression ‘Lease’ under the Stamp Act has a wider meaning compared to its original meaning under Section 105 of the Transfer of Property Act. If ‘Lease’ under Section 2(16) of the Stamp Act includes specified categories of documents, it shows an intention to extend the definition beyond traditional leases of immovable property.”

The Court emphasized:

- Section 2(16)(c) of the Indian Stamp Act specifically includes agreements for toll collection as leases.

- The contracts created enforceable rights and liabilities, granting the contractors a financial interest akin to a leaseholder.

- The nature of the agreements showed that the contractors were not merely acting as municipal agents but had independent rights to collect fees.

- The New Bus-Stand Shop Owners Association case was not applicable, as it dealt with shop rental agreements rather than toll collection contracts.

Final Verdict

The Supreme Court:

- Upheld the Allahabad High Court’s ruling.

- Declared that contracts for collecting Tehbazari and parking fees were leases under the Indian Stamp Act.

- Directed the contractors to pay the requisite stamp duty as determined by the Collector of Stamps.

- Rejected the argument that these contracts were mere licenses.

Impact of the Judgment

This ruling has significant implications for municipal revenue collection and the classification of government contracts:

- Clarifies the taxation of municipal contracts: Ensures that stamp duty is correctly assessed on agreements involving fee collection rights.

- Prevents revenue loss: Ensures that governments collect the appropriate duty from toll collection contracts.

- Sets a precedent for similar agreements: Other states may follow this ruling in classifying municipal fee collection contracts.

- Protects public revenue: Ensures that contractors do not evade tax obligations by misclassifying agreements.

The Supreme Court’s ruling strengthens the government’s ability to regulate and collect revenue from municipal contracts, reinforcing the broader principle that all contracts granting financial interests should be subject to proper stamp duty regulations.

Don’t miss out on the full details! Download the complete judgment in PDF format below and gain valuable insights instantly!

Download Judgment: Nasiruddin & Anr. vs The State of Uttar P Supreme Court of India Judgment Dated 06-12-2017.pdf

Direct Downlaod Judgment: Direct downlaod this Judgment

See all petitions in Contract Disputes

See all petitions in Debt Recovery

See all petitions in Specific Performance

See all petitions in Judgment by Abhay Manohar Sapre

See all petitions in Judgment by Navin Sinha

See all petitions in dismissed

See all petitions in supreme court of India judgments December 2017

See all petitions in 2017 judgments

See all posts in Civil Cases Category

See all allowed petitions in Civil Cases Category

See all Dismissed petitions in Civil Cases Category

See all partially allowed petitions in Civil Cases Category