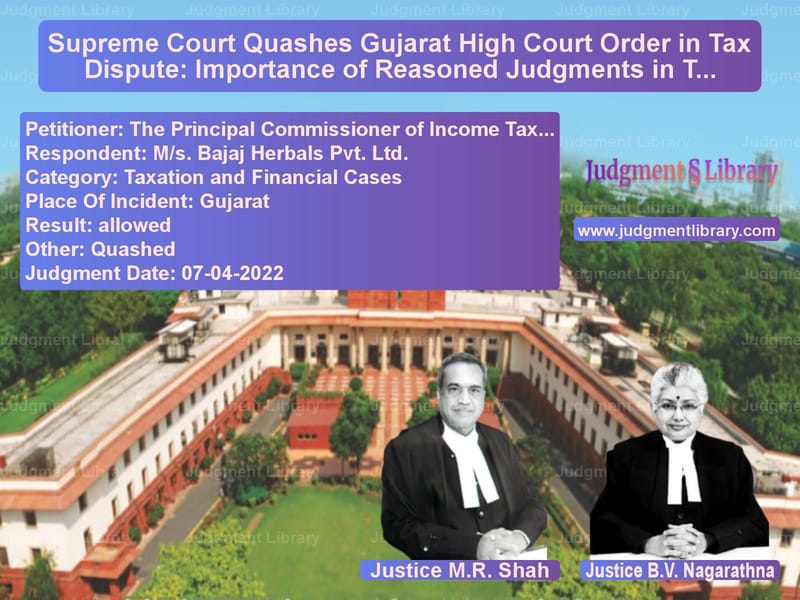

Supreme Court Quashes Gujarat High Court Order in Tax Dispute: Importance of Reasoned Judgments in Tax Appeals

The case of The Principal Commissioner of Income Tax-1 vs. M/s. Bajaj Herbals Pvt. Ltd. raised crucial questions regarding the duty of appellate courts to provide a reasoned judgment when dismissing tax appeals. The Supreme Court found that the Gujarat High Court dismissed the Revenue Department’s appeal without adequate reasoning, thereby failing to determine whether substantial questions of law were involved. As a result, the Supreme Court quashed the High Court’s order and remanded the matter for fresh adjudication.

Background of the Case

The dispute arose when the Revenue Department filed an appeal against M/s. Bajaj Herbals Pvt. Ltd., challenging the Gujarat High Court’s summary dismissal of the department’s plea. The central issue in the case was whether the High Court had erred in failing to consider and provide reasons for dismissing a tax appeal that raised substantial questions of law.

Key developments in the case:

- October 1, 2020: The Gujarat High Court dismissed the Revenue Department’s appeal, stating that the questions proposed by the department were not “substantial questions of law.”

- December 2, 2020: The High Court modified its order but did not provide any detailed reasoning for rejecting the appeal.

- 2021: The Revenue Department, dissatisfied with the High Court’s approach, filed a Special Leave Petition (SLP) before the Supreme Court.

Petitioners’ Arguments

The Additional Solicitor General Balbir Singh, representing the Revenue Department, argued:

“The Gujarat High Court dismissed the appeal without assigning any substantial reasoning. A mere statement that ‘no substantial question of law arises’ is insufficient. The High Court must engage with the legal and factual contentions raised by the parties before rejecting an appeal outright.”

The Revenue Department raised the following key points:

- The appeal involved complex questions of income tax law interpretation that should have been examined by the High Court.

- The High Court’s judgment lacked proper reasoning, making it a non-speaking order in violation of established legal principles.

- The failure to articulate reasons for dismissal meant that the order was arbitrary and against the principles of natural justice.

- By failing to discuss the specific provisions of the Income Tax Act and how they applied to the case, the High Court had effectively denied the Revenue Department a fair hearing.

- The Supreme Court, in multiple precedents, had emphasized that appellate courts must provide reasoned orders to ensure judicial transparency and accountability.

Respondents’ Arguments

The respondent, M/s. Bajaj Herbals Pvt. Ltd., did not appear before the Supreme Court despite being served notice. The Court took note of this absence and stated:

“Despite granting sufficient time, no one has appeared on behalf of the respondent. The service of notice is deemed complete.”

However, the Supreme Court proceeded to evaluate the case on its merits, relying on the arguments presented by the Revenue Department.

Supreme Court’s Observations

The Supreme Court bench, comprising Justices M.R. Shah and B.V. Nagarathna, ruled in favor of the Revenue Department and set aside the Gujarat High Court’s order.

The Court emphasized the duty of appellate courts to provide reasoned judgments when dismissing tax appeals. It observed:

“The High Court has merely recorded that ‘none of the questions as proposed by the Revenue could be termed as substantial questions of law.’ There is no independent reasoning given to justify this conclusion.”

The Court identified the following deficiencies in the High Court’s approach:

- The High Court failed to analyze whether the issues raised by the Revenue involved substantial questions of law.

- It did not provide any reasoning for concluding that the appeal lacked merit.

- The dismissal order lacked judicial transparency, as it did not explain why the appeal was unworthy of consideration.

- The Gujarat High Court had an obligation to provide a speaking order instead of summarily rejecting the appeal.

Legal Precedents Considered

The Supreme Court referred to several precedents to support its decision:

- Kotak Mahindra Bank Ltd. vs. Hindustan National Glass & Industries Ltd. (2021): Emphasized that courts must provide reasoned orders to ensure fairness in judicial decisions.

- Assistant Commissioner of Income Tax vs. Rajesh Jhaveri Stock Brokers Pvt. Ltd. (2007): Stressed that tax matters involving complex legal interpretations should not be summarily dismissed.

- Union of India vs. Ibrahim Uddin (2012): Held that non-speaking orders violate the principles of natural justice.

Final Ruling

The Supreme Court quashed the Gujarat High Court’s order and ruled:

- The matter is remanded to the Gujarat High Court for fresh adjudication.

- The High Court must pass a speaking and reasoned order, addressing the Revenue’s arguments.

- The High Court shall determine whether the questions raised by the Revenue qualify as “substantial questions of law.”

Conclusion

The Supreme Court’s ruling underscores the importance of reasoned judgments in tax appeals. The decision ensures that appellate courts cannot dismiss tax cases arbitrarily and must provide well-reasoned explanations before rejecting appeals. This judgment sets a precedent for greater judicial accountability and fairness in tax litigation.

Read also: https://judgmentlibrary.com/amalgamated-companies-and-tax-liability-supreme-courts-key-ruling/

Petitioner Name: The Principal Commissioner of Income Tax-1.Respondent Name: M/s. Bajaj Herbals Pvt. Ltd..Judgment By: Justice M.R. Shah, Justice B.V. Nagarathna.Place Of Incident: Gujarat.Judgment Date: 07-04-2022.

Don’t miss out on the full details! Download the complete judgment in PDF format below and gain valuable insights instantly!

Download Judgment: the-principal-commis-vs-ms.-bajaj-herbals-p-supreme-court-of-india-judgment-dated-07-04-2022.pdf

Directly Download Judgment: Directly download this Judgment

See all petitions in Income Tax Disputes

See all petitions in Tax Refund Disputes

See all petitions in Banking Regulations

See all petitions in Judgment by Mukeshkumar Rasikbhai Shah

See all petitions in Judgment by B.V. Nagarathna

See all petitions in allowed

See all petitions in Quashed

See all petitions in supreme court of India judgments April 2022

See all petitions in 2022 judgments

See all posts in Taxation and Financial Cases Category

See all allowed petitions in Taxation and Financial Cases Category

See all Dismissed petitions in Taxation and Financial Cases Category

See all partially allowed petitions in Taxation and Financial Cases Category