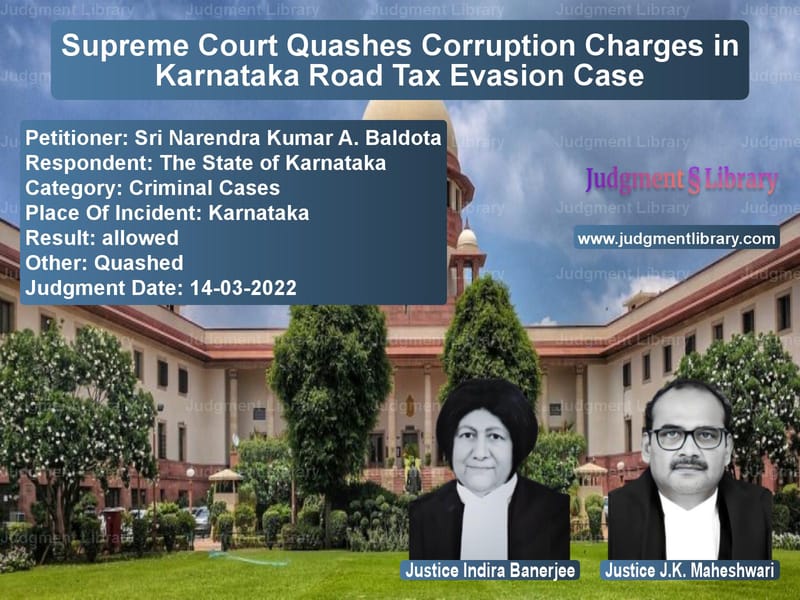

Supreme Court Quashes Corruption Charges in Karnataka Road Tax Evasion Case

The Supreme Court of India recently delivered a crucial judgment in the case of Sri Narendra Kumar A. Baldota vs. The State of Karnataka, where it quashed criminal proceedings against the petitioner in a corruption and tax evasion case related to luxury car imports. The judgment reinforces legal principles on corporate liability, tax compliance, and misuse of criminal law.

Background of the Case

The case stemmed from allegations of large-scale tax evasion in Karnataka, where multiple high-end vehicles were reportedly registered at undervalued prices to evade road tax. The petitioner, Sri Narendra Kumar A. Baldota, was named in an FIR alleging that he conspired with transport officials to underpay taxes on an Aston Martin Rapide, leading to a shortfall of Rs. 20,44,468 in road tax payments.

The prosecution alleged that MSPL Limited, a company chaired by the petitioner, had undervalued the vehicle while registering it. Following a complaint, the Lokayukta police launched an investigation, leading to criminal charges under the Prevention of Corruption Act and the Indian Penal Code.

Key Legal Issues Considered

- Whether the petitioner, as the company’s chairman, could be held personally liable for the alleged tax evasion.

- Whether criminal proceedings were justified when the tax shortfall was later paid in full.

- Whether the Karnataka High Court erred in rejecting the petitioner’s plea for quashing the proceedings.

Petitioner’s Arguments (Sri Narendra Kumar A. Baldota)

- The petitioner was neither the registered owner of the vehicle nor directly responsible for its registration.

- MSPL Limited followed all prescribed legal procedures for the vehicle’s import and registration.

- The disputed road tax was paid in full after receiving a demand notice from the RTO.

- The case was politically motivated and aimed at harassing corporate executives.

- The High Court failed to recognize that the tax issue was purely administrative and did not warrant criminal prosecution.

Respondent’s Arguments (State of Karnataka)

- The prosecution maintained that the vehicle was deliberately undervalued to reduce tax liability.

- The petitioner, as the head of MSPL Limited, was accountable for financial decisions, including tax payments.

- Despite later payment of the tax, the original intent to evade liability constituted an offense under the law.

- The charges involved corruption and required full trial proceedings before any exoneration.

Supreme Court’s Observations

- The Court noted that the petitioner was not personally responsible for vehicle registration.

- The tax shortfall had been paid before the criminal proceedings, resolving any outstanding liability.

- No evidence suggested that the petitioner had committed fraud or conspired with officials.

- The criminal case was deemed an abuse of legal process aimed at corporate harassment.

The Court stated:

“Criminal proceedings should not be used as a tool to coerce individuals or companies into compliance when tax-related issues can be addressed administratively.”

Final Judgment

- The Supreme Court quashed all criminal proceedings against the petitioner.

- The High Court’s dismissal of the quashing petition was overturned.

- The ruling confirmed that corporate executives cannot be held criminally liable for routine financial discrepancies without evidence of wrongdoing.

Key Takeaways from the Judgment

- Corporate liability should be clearly defined: Company executives should not face criminal charges without direct involvement in alleged offenses.

- Administrative tax issues do not warrant criminal prosecution: The Court emphasized that road tax shortfalls, once rectified, should not lead to criminal cases.

- Prevention of legal harassment: The judgment discourages misuse of criminal law to target individuals without substantial proof.

Conclusion

The Supreme Court’s ruling in this case strengthens protections for corporate executives against frivolous criminal charges and reinforces the principle that tax compliance should be handled through administrative processes rather than coercive legal actions. This decision sets an important precedent for future tax-related legal disputes in India.

Read also: https://judgmentlibrary.com/supreme-court-cancels-bail-in-puran-mal-vs-state-of-haryana-murder-case/

Petitioner Name: Sri Narendra Kumar A. Baldota.Respondent Name: The State of Karnataka.Judgment By: Justice Indira Banerjee, Justice J.K. Maheshwari.Place Of Incident: Karnataka.Judgment Date: 14-03-2022.

Don’t miss out on the full details! Download the complete judgment in PDF format below and gain valuable insights instantly!

Download Judgment: sri-narendra-kumar-a-vs-the-state-of-karnata-supreme-court-of-india-judgment-dated-14-03-2022.pdf

Directly Download Judgment: Directly download this Judgment

See all petitions in Fraud and Forgery

See all petitions in Extortion and Blackmail

See all petitions in Money Laundering Cases

See all petitions in Bail and Anticipatory Bail

See all petitions in Public Interest Litigation

See all petitions in Judgment by Indira Banerjee

See all petitions in Judgment by J.K. Maheshwari

See all petitions in allowed

See all petitions in Quashed

See all petitions in supreme court of India judgments March 2022

See all petitions in 2022 judgments

See all posts in Criminal Cases Category

See all allowed petitions in Criminal Cases Category

See all Dismissed petitions in Criminal Cases Category

See all partially allowed petitions in Criminal Cases Category