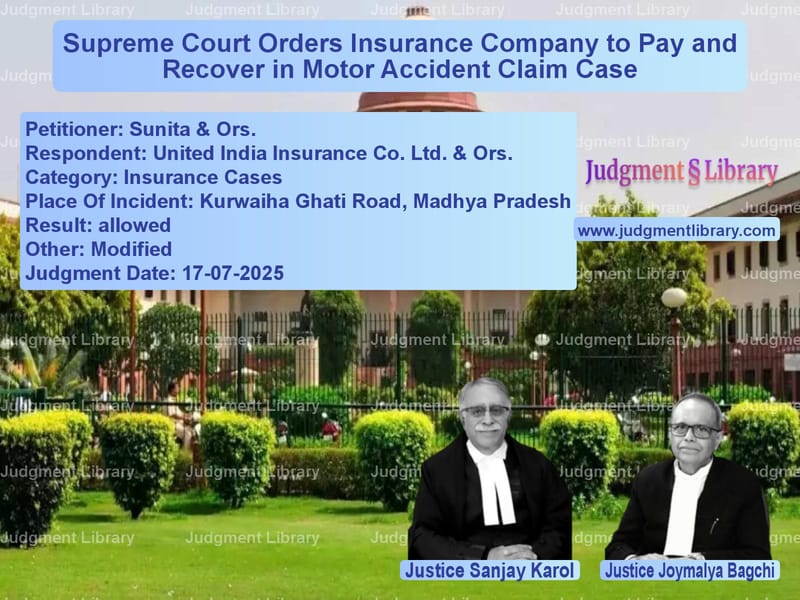

Supreme Court Orders Insurance Company to Pay and Recover in Motor Accident Claim Case

In a landmark judgment that reinforces the principle of protecting accident victims, the Supreme Court of India recently delivered a significant ruling that clarifies the liability of insurance companies in motor accident claims involving policy violations. The case involved Sunita and other legal representatives of Gokul Prasad, who tragically lost his life in a road accident, and their fight for compensation against United India Insurance Company Ltd.

The tragic incident occurred on November 27, 2013, around 8:15 PM, when Gokul Prasad, a 32-year-old cloth seller, was returning home from a weekly market. He was travelling in a TATA 407 Truck bearing registration No. M.P. 53G/0386, driven by Respondent No. 3. As the vehicle reached near Kurwaiha Ghati Road, it met with an accident due to rash and negligent driving, resulting in Gokul Prasad sustaining severe injuries and dying on the spot.

The legal representatives of the deceased filed a claim petition under Section 166 of the Motor Vehicles Act, 1988, before the Motor Accident Claim Tribunal, District Seedhi, Madhya Pradesh. They sought compensation of Rs. 49,26,000, claiming that the deceased earned Rs. 12,000 per month as a cloth seller. The Insurance Company opposed the claim, arguing that there was a breach of policy conditions since the offending vehicle was being used as a loading vehicle without a valid permit, registration, and fitness certificate. Additionally, they contended that the driver did not hold a valid license, and therefore, the Insurance Company should not be liable to pay any compensation.

The Tribunal, in its order dated December 19, 2016, awarded compensation of Rs. 19,53,000 with interest at 6% per annum. However, the liability to pay compensation was fastened solely upon the driver and owner of the vehicle, citing clear violation of the terms and conditions of the insurance policy. The Tribunal held that although the vehicle was commercial in nature, the driver possessed a license only to drive a Light Motor Vehicle (non-commercial vehicle) without the necessary endorsement to drive a commercial vehicle. The Tribunal also noted that the vehicle was insured under a “Liability Only Policy” that covered only third-party liability, with no premium paid to cover the driver or owner of the vehicle.

The owner of the offending vehicle appealed to the High Court of Madhya Pradesh at Jabalpur, which dismissed the appeal through its order dated December 12, 2022. The High Court affirmed the compensation awarded by the Tribunal and agreed that the Insurance Company was rightly exonerated, with liability remaining with the driver and owner. The High Court relied on Mukund Dewangan v. Oriental Insurance Company Ltd., holding that no endorsement was required to drive a commercial vehicle if the driver held a license to drive a Light Motor Vehicle. However, the Court also referenced New India Assurance Company Ltd. v. Vedwati and New India Assurance Company Ltd. v. Asharani, concluding that since no premium was paid to cover the liability of the driver or any passenger travelling, the Insurance Company’s liability was correctly excluded.

The present appeal was instituted by the claimant-appellants before the Supreme Court, with the significant ground of challenge being that the Courts below should have adopted the principle of “pay and recover” as established in National Insurance Co. Ltd. v. Paravathneni & Anr., where the Insurance Company was directed to initially pay compensation to the claimants and then recover it from the insured.

The Supreme Court, comprising Justices Sanjay Karol and Joymalya Bagchi, heard arguments from the parties and also received assistance from learned amicus curiae Ms. Vidhi Pankaj Thaker, who prepared a calculation chart indicating just and fair compensation for the claimant-appellants.

The Court first addressed the issue of the driver’s license. The findings of the Courts below revealed that the driver held a valid license to drive a Light Motor Vehicle, while the vehicle in question was a commercial one. The Supreme Court agreed with the High Court’s view that no endorsement was required to drive the commercial vehicle, citing the recent Constitutional Bench decision in Bajaj Alliance General Insurance Co. Ltd. v. Rambha Devi, which affirmed the three-Judge Bench view in Mukund Dewangan. The Court noted: “A driver holding a licence for light motor vehicle (LMV) class, under Section 10(2) (d) for vehicles with a gross vehicle weight under 7500 kg, is permitted to operate a ‘transport vehicle’ without needing additional authorisation under Section 10(2)(e) of the MV Act specifically for the ‘transport vehicle’ class.”

The Supreme Court observed: “Thus, in our considered view, in the present case, although the offending vehicle is a commercial one and the driver of the said vehicle at the time of accident possessed a license to only drive a Light Motor Vehicle (LMV) and, considering the gross weight of the vehicle in question is not in excess of 7500 Kg., the driver can be said to be holding a valid license to drive the same.”

The Court then addressed the crucial question of whether the Insurance Company could be held liable despite the policy limitations. The Court noted that the vehicle was insured with a “Liability Only Policy” and no premium was paid to cover the driver, owner, or gratuitous passenger. However, the Supreme Court found that the Courts below erred in holding that the Insurance Company was not liable to pay compensation, stating that the principle of “Pay and Recover” should have been invoked.

The Supreme Court referenced its exposition in National Insurance Co. Ltd. v. Baljit Kaur, where the deceased was travelling as a gratuitous passenger and the Insurance Company was directed to satisfy the awarded amount and recover it from the vehicle owner since no premium was paid towards gratuitous passengers. This position was followed in Anu Bhanvara v. IFFCO Tokio General Insurance Co. Ltd., where the principle of “Pay and Recover” was applied, directing the Insurance Company to pay the amount and then recover it from the vehicle owner.

The Court noted: “The aforementioned principle was adopted by this Court in various judgments of this Court in Amrit Lal Sood v. Kaushalya Devi Thapar; New India Assurance Co. Ltd. v. C.M. Jaya; National Insurance Co. Ltd. v. Challa Upendra Rao; New India Assurance Co. Ltd. v. Vimal Devi; National Insurance Co. Ltd. v. Saju P. Paul; Manuara Khatun v. Rajesh Kumar Singh; and Puttappa v. Rama Naik.”

The Supreme Court held: “Applying the above expositions of law, the Courts below ought to have directed the Insurance Company to indemnify the amount and thereafter recover the same. Therefore, in light of the attending facts and circumstances of the case, we are of the view that the Insurance Company is liable to indemnify the compensation amount awarded by the Tribunal and recover the same only from the owner of the offending vehicle.”

Regarding the compensation amount, the Court concurred with the assessment of the deceased’s monthly income at Rs. 12,000 but increased the amount awarded under conventional heads – loss of estate, loss of consortium, and funeral expenses – by 10%, following the principle laid down in National Insurance Co. Ltd. v. Pranay Sethi that such amounts should be revised every three years.

The Supreme Court recalculated the compensation as follows: Monthly income of Rs. 12,000; yearly income of Rs. 1,44,000; future prospects of 40% (since the deceased was 32 years old) bringing it to Rs. 2,01,600; after 1/4 deduction, Rs. 1,51,200; multiplied by 16 (multiplier for age 32) giving Rs. 24,19,200 for loss of income; plus Rs. 18,150 for loss of estate; Rs. 18,150 for funeral expenses; and Rs. 2,42,000 for loss of consortium (Rs. 48,400 multiplied by 5 with 10% increase every three years from 2017). The total compensation awarded was Rs. 26,97,500, significantly higher than the Rs. 19,53,000 awarded by the Tribunal and High Court.

The Supreme Court allowed the appeal and directed: “Let the amount be directly remitted into the bank account of the claimant-appellant(s). The particulars of the bank account are to be immediately supplied by the learned counsel for the appellant(s) to the learned counsel for the respondent. The amount be remitted positively within a period of four weeks thereafter.”

This judgment reinforces the Supreme Court’s consistent approach of prioritizing the interests of accident victims while balancing the rights of insurance companies through the “pay and recover” principle. The ruling ensures that victims and their families receive timely compensation while allowing insurance companies to recover amounts from responsible parties in cases of policy violations, thus serving the dual purpose of victim protection and contractual enforcement.

Petitioner Name: Sunita & Ors..Respondent Name: United India Insurance Co. Ltd. & Ors..Judgment By: Justice Sanjay Karol, Justice Joymalya Bagchi.Place Of Incident: Kurwaiha Ghati Road, Madhya Pradesh.Judgment Date: 17-07-2025.Result: allowed.

Don’t miss out on the full details! Download the complete judgment in PDF format below and gain valuable insights instantly!

Download Judgment: sunita-&-ors.-vs-united-india-insuran-supreme-court-of-india-judgment-dated-17-07-2025.pdf

Directly Download Judgment: Directly download this Judgment

See all petitions in Motor Insurance Settlements

See all petitions in Insurance Settlements

See all petitions in Compensation Disputes

See all petitions in Road Accident Cases

See all petitions in Judgment by Sanjay Karol

See all petitions in Judgment by Joymalya Bagchi

See all petitions in allowed

See all petitions in Modified

See all petitions in supreme court of India judgments July 2025

See all petitions in 2025 judgments

See all posts in Insurance Cases Category

See all allowed petitions in Insurance Cases Category

See all Dismissed petitions in Insurance Cases Category

See all partially allowed petitions in Insurance Cases Category