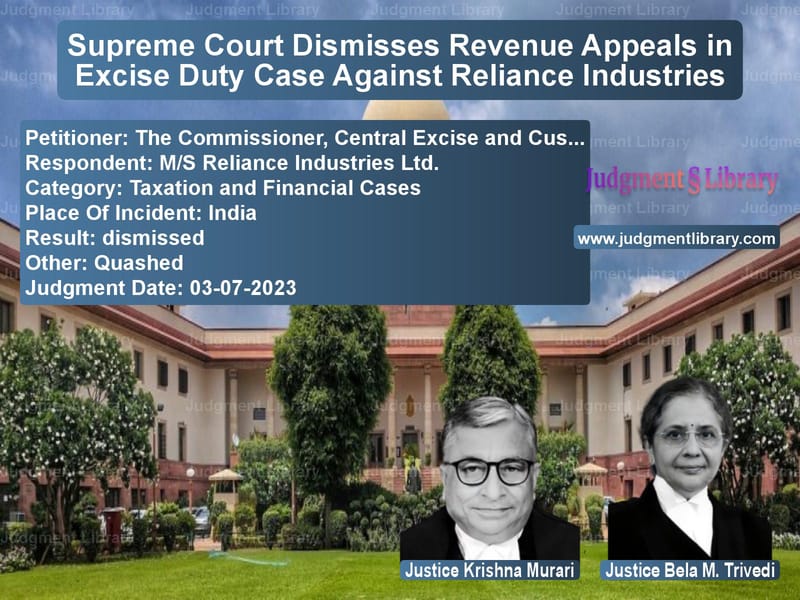

Supreme Court Dismisses Revenue Appeals in Excise Duty Case Against Reliance Industries

The case of The Commissioner, Central Excise and Customs v. M/S Reliance Industries Ltd. is a landmark ruling where the Supreme Court ruled in favor of Reliance Industries Ltd. (RIL), dismissing the appeals filed by the Revenue Department. The Court held that the excise duty demand raised by the department was time-barred and could not be sustained. This decision clarifies the application of the extended limitation period under Section 11A of the Central Excise Act, 1944, and provides clarity on revenue neutrality in taxation cases.

Background of the Case

The Revenue Department issued a show cause notice to RIL on September 28, 2005, demanding differential excise duty on clearances made from September 2000 to March 2004. The demand was based on the allegation that RIL had incorrectly determined the assessable value of its finished goods by not including the monetary value of duty benefits transferred to its customers.

The Commissioner of Central Excise, Rajkot, confirmed the demand under the extended period of limitation under the proviso to Section 11A(1) of the Central Excise Act, 1944. However, RIL appealed to the Customs, Excise & Service Tax Appellate Tribunal (CESTAT), which ruled in its favor on March 17, 2009, declaring the demand time-barred.

The Revenue Department then challenged the CESTAT order before the Supreme Court.

Key Legal Issues

- Was the demand for excise duty time-barred under Section 11A(1) of the Central Excise Act?

- Did RIL suppress material facts to evade duty, justifying the invocation of the extended limitation period?

- Did the concept of revenue neutrality apply in this case?

Petitioner’s (Revenue Department’s) Arguments

The Revenue Department, represented by its counsel, argued:

- RIL had willfully suppressed relevant facts by not including duty benefits in the assessable value of goods.

- The extended limitation period of five years was justified under the proviso to Section 11A(1) since RIL engaged in intentional non-disclosure.

- The company’s argument of revenue neutrality was flawed because duty evasion resulted in loss to the government.

- The CESTAT’s reliance on revenue neutrality ignored the fact that the customers’ ability to claim CENVAT credit did not absolve RIL of its duty obligations.

Respondent’s (Reliance Industries Ltd.) Arguments

RIL, represented by its counsel, countered:

- The company had acted in good faith based on the prevailing CESTAT ruling in IFGL Refractories Ltd. (2001), which was later overturned by the Supreme Court in 2005.

- The extended limitation period did not apply because RIL did not suppress any material facts; all transactions were recorded and disclosed to the department.

- The excise duty demand was revenue-neutral since RIL’s customers were eligible to claim input tax credit.

- The CESTAT’s ruling on time-bar was consistent with judicial precedents in Pushpam Pharmaceuticals (1995) and Chemphar Drugs & Liniments (1989), which held that suppression must involve deliberate intent to evade duty.

Supreme Court’s Observations

On the Extended Limitation Period

The Supreme Court ruled that the extended limitation period could not be invoked as there was no deliberate suppression of facts by RIL. The Court stated:

“The expression ‘suppression of facts’ in Section 11A must be read in the context of fraud, collusion, or willful misstatement. It does not apply to mere failure to disclose information when the department had access to all relevant records.”

On Revenue Neutrality

The Court accepted RIL’s contention that the transactions were revenue-neutral since the company’s customers could claim CENVAT credit on any additional duty paid. It held:

“In a self-assessment regime, where customers are eligible for input tax credit, any additional duty payment would be offset by a corresponding credit. Therefore, there is no loss of revenue to the exchequer.”

On the CESTAT Ruling in IFGL Refractories

The Court found merit in RIL’s argument that it had followed the prevailing CESTAT ruling at the time and could not have foreseen its reversal by the Supreme Court in 2005. The Court noted:

“Between 2000 and 2005, the assessee acted in accordance with the law as interpreted by the Tribunal. The subsequent reversal of this ruling does not render the assessee’s belief mala fide.”

Final Judgment

The Supreme Court dismissed the appeals filed by the Revenue Department, ruling:

- The demand for excise duty was time-barred and unenforceable.

- RIL had not engaged in willful suppression of facts.

- The revenue neutrality principle applied, negating the duty demand.

- The ruling in IFGL Refractories provided a valid basis for RIL’s compliance.

Implications of the Judgment

This ruling has far-reaching implications:

- Clarifies Time Limits for Excise Duty Demands: Reaffirms that the extended limitation period under Section 11A cannot be invoked in the absence of intent to evade duty.

- Strengthens Revenue Neutrality Doctrine: Recognizes that duty demands should consider the availability of input tax credits.

- Ensures Legal Certainty for Taxpayers: Protects businesses from retrospective tax demands based on later judicial decisions.

Conclusion

The Supreme Court’s ruling in The Commissioner, Central Excise and Customs v. M/S Reliance Industries Ltd. reinforces the principle that tax assessments must be conducted within prescribed time limits. The judgment underscores the importance of good faith compliance and prevents retrospective penalties based on changing legal interpretations.

Petitioner Name: The Commissioner, Central Excise and Customs.Respondent Name: M/S Reliance Industries Ltd..Judgment By: Justice Krishna Murari, Justice Bela M. Trivedi.Place Of Incident: India.Judgment Date: 03-07-2023.

Don’t miss out on the full details! Download the complete judgment in PDF format below and gain valuable insights instantly!

Download Judgment: the-commissioner,-ce-vs-ms-reliance-industr-supreme-court-of-india-judgment-dated-03-07-2023.pdf

Directly Download Judgment: Directly download this Judgment

See all petitions in Tax Refund Disputes

See all petitions in Customs and Excise

See all petitions in Judgment by Krishna Murari

See all petitions in Judgment by Bela M. Trivedi

See all petitions in dismissed

See all petitions in Quashed

See all petitions in supreme court of India judgments July 2023

See all petitions in 2023 judgments

See all posts in Taxation and Financial Cases Category

See all allowed petitions in Taxation and Financial Cases Category

See all Dismissed petitions in Taxation and Financial Cases Category

See all partially allowed petitions in Taxation and Financial Cases Category