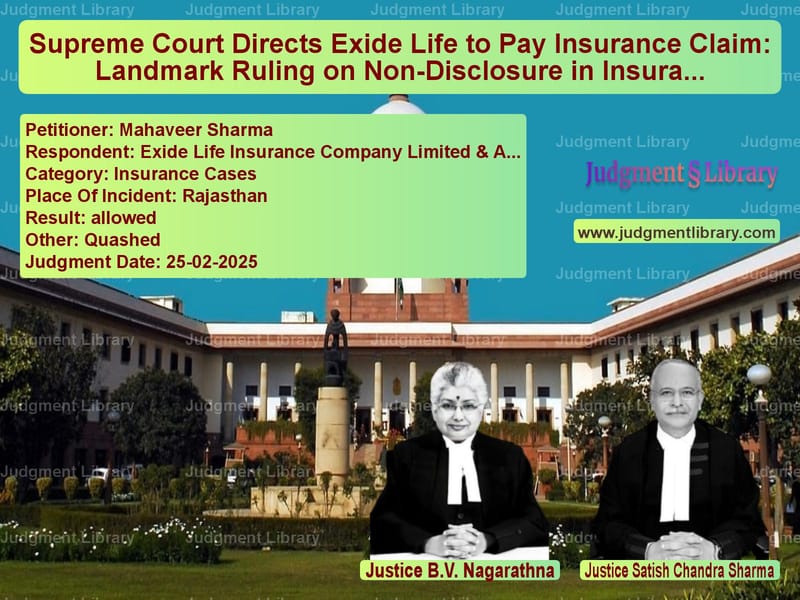

Supreme Court Directs Exide Life to Pay Insurance Claim: Landmark Ruling on Non-Disclosure in Insurance Policies

In a significant ruling, the Supreme Court of India has set aside the repudiation of an insurance claim by Exide Life Insurance Company Limited, holding that a mere non-disclosure of certain insurance policies does not amount to material suppression if the insurer was already aware of a higher-value policy held by the insured. The Court directed Exide Life to release all benefits under the policy with 9% interest per annum.

Background of the Case

The case arose when the appellant, Mahaveer Sharma, filed a claim for insurance benefits following the accidental death of his father, Ramkaran Sharma, who had taken a life insurance policy from Exide Life on June 9, 2014. However, Exide Life repudiated the claim on March 3, 2016, citing material suppression—stating that the deceased had failed to disclose all of his existing life insurance policies when applying for the Exide Life policy.

The appellant challenged the repudiation before the State Consumer Disputes Redressal Commission, Rajasthan, which dismissed the complaint. His subsequent appeal to the National Consumer Disputes Redressal Commission (NCDRC) was also dismissed on May 28, 2019. Finally, he approached the Supreme Court, challenging the rejection of his claim.

Legal Issues

- Whether the non-disclosure of other life insurance policies amounts to material suppression sufficient to repudiate a claim.

- Whether an insurance company can deny claims for non-disclosure when the insured had disclosed another high-value policy.

- The interpretation of ‘material facts’ in insurance contracts and their relevance in claim repudiation.

Arguments by the Appellant

The appellant’s counsel argued:

- The deceased had disclosed an Aviva Life Insurance policy of Rs. 40 lakhs, but inadvertently did not mention three smaller policies from the Life Insurance Corporation of India.

- The omission was unintentional and did not impact the insurer’s decision to issue the policy.

- The death occurred due to an accident, not due to any pre-existing medical condition that might have required disclosure.

- The proposal form was filled out by an insurance agent, and the insured had provided all necessary details.

“The failure to mention three small-value policies while disclosing a much larger policy should not be considered a material suppression warranting claim repudiation.”

Arguments by the Respondents

Exide Life Insurance countered:

- Failure to disclose all existing insurance policies constituted material suppression, justifying claim repudiation.

- The insurer must have complete information about all existing policies to assess risk properly.

- The insured was contractually obligated to disclose all policies, irrespective of the sum assured.

“The suppression of material facts, even if inadvertent, affects the insurer’s ability to evaluate risk and must be treated seriously.”

Supreme Court’s Observations

The Supreme Court carefully examined the case and observed:

- The insured had made a substantial disclosure by mentioning the Aviva Life policy worth Rs. 40 lakhs.

- The omitted policies were of lower value (aggregating Rs. 2.3 lakhs) and would not have materially affected the insurer’s risk assessment.

- The insurer had access to the disclosed Aviva policy details and could have sought additional information if needed.

- The failure to disclose the LIC policies did not influence the insurer’s decision, making the repudiation unjustified.

“The insurer was aware of a larger policy and did not seek clarification on other policies. Repudiating the claim on such technical grounds is improper.”

Final Judgment

The Supreme Court ruled:

“The order of repudiation dated 03.03.2016, the order of the National Commission dated 28.05.2019, and the order of the State Commission dated 27.09.2018 are set aside. The respondent insurance company is directed to release all benefits under the policy along with interest of 9% per annum from the date the amount became due till the date of realization.”

This ruling ensures that insurance companies cannot reject claims based on minor technical omissions when a substantial disclosure has been made.

Impact of the Judgment

This ruling has significant implications for insurance policyholders:

- It establishes that non-disclosure of minor policies does not automatically constitute material suppression.

- It reinforces that insurers cannot deny claims arbitrarily when a substantial disclosure has been made.

- It highlights the duty of insurers to verify policyholder information before rejecting claims.

- It ensures greater consumer protection in insurance contracts.

By directing Exide Life to honor the claim, the Supreme Court has reinforced the principle that insurance companies must act fairly and transparently in assessing claims.

Petitioner Name: Mahaveer Sharma.Respondent Name: Exide Life Insurance Company Limited & Another.Judgment By: Justice B.V. Nagarathna, Justice Satish Chandra Sharma.Place Of Incident: Rajasthan.Judgment Date: 25-02-2025.

Don’t miss out on the full details! Download the complete judgment in PDF format below and gain valuable insights instantly!

Download Judgment: mahaveer-sharma-vs-exide-life-insurance-supreme-court-of-india-judgment-dated-25-02-2025.pdf

Directly Download Judgment: Directly download this Judgment

See all petitions in Life Insurance Claims

See all petitions in Insurance Settlements

See all petitions in Judgment by B.V. Nagarathna

See all petitions in Judgment by Satish Chandra Sharma

See all petitions in allowed

See all petitions in Quashed

See all petitions in supreme court of India judgments February 2025

See all petitions in 2025 judgments

See all posts in Insurance Cases Category

See all allowed petitions in Insurance Cases Category

See all Dismissed petitions in Insurance Cases Category

See all partially allowed petitions in Insurance Cases Category