Jewelry Insurance Claim Rejected: Supreme Court Rules on Policy Exclusions

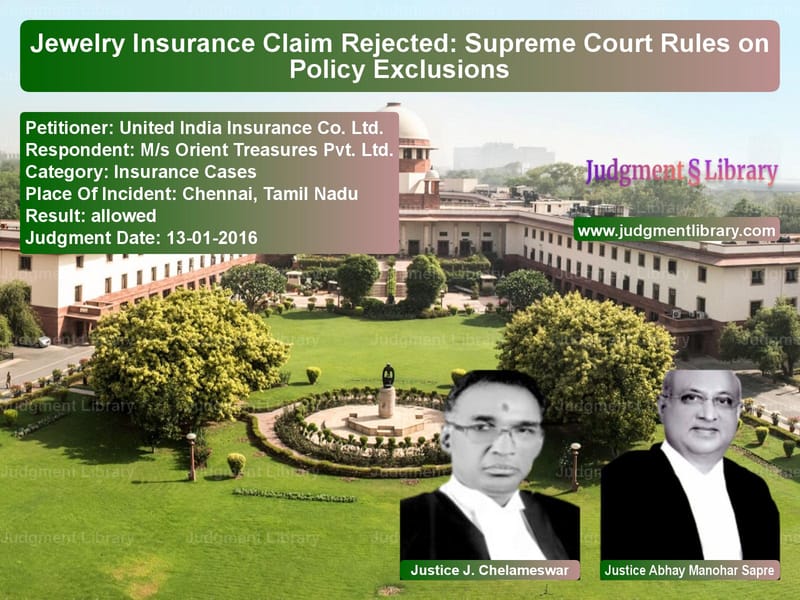

The case of United India Insurance Co. Ltd. v. M/s Orient Treasures Pvt. Ltd. revolves around a significant legal issue concerning insurance claims and policy exclusions. The Supreme Court of India examined whether an insurance company was liable to compensate for a burglary claim when the stolen items were explicitly excluded under the terms of the policy. The ruling emphasizes the importance of carefully understanding policy terms before making claims.

Background of the Case

The dispute arose when M/s Orient Treasures Pvt. Ltd., a jewelry business, filed a claim with United India Insurance Co. Ltd. after a burglary occurred at its store. The insured jewelry store, operating under the name “Kanchana Mahal” in Chennai, had an active ‘Jewellers Block Policy’ from United India Insurance, covering its stock of gold and silver ornaments.

On the night of June 2, 1995, burglars broke into the shop and allegedly stole jewelry valued at Rs. 40,63,735.53. The respondent (Orient Treasures Pvt. Ltd.) reported the incident to the police and the insurance company on June 3, 1995. Following an investigation, the police marked the case as ‘untraceable.’

Insurance Claim and Denial

After the burglary, the insured party submitted a claim for compensation under the insurance policy. However, United India Insurance repudiated the claim on January 19, 1998, stating that the stolen items were left outside the safe and in the display window, which was explicitly excluded from coverage as per policy conditions.

Legal Proceedings

Complaint Before Consumer Commission

Unhappy with the rejection of the claim, M/s Orient Treasures Pvt. Ltd. filed a complaint before the National Consumer Disputes Redressal Commission (NCDRC), seeking compensation of Rs. 1,32,06,786.30. The Commission, after reviewing the case, partially allowed the complaint and directed United India Insurance to pay Rs. 36,10,211 with 10% interest per annum from December 3, 1995, along with Rs. 50,000 as litigation costs.

Appeal to the Supreme Court

Both parties were dissatisfied with the NCDRC ruling and filed appeals before the Supreme Court:

- United India Insurance challenged the compensation award, arguing that the policy terms clearly excluded coverage for items kept outside the safe at night.

- M/s Orient Treasures Pvt. Ltd. filed a counter-appeal seeking an enhancement of the awarded compensation.

Arguments Presented

Insurance Company’s Arguments

- The insurer argued that clauses 4, 5, and 12 of the policy explicitly stated that jewelry left outside the safe or in window displays after business hours was not covered.

- The burglary occurred at night, and stolen items were not stored in the safe, making the claim ineligible.

- They relied on past Supreme Court rulings that emphasized clear policy exclusions must be enforced.

Policyholder’s Arguments

- The complainant contended that they had paid premiums for comprehensive coverage of their jewelry, and a burglary should not be denied compensation based on technical policy exclusions.

- They argued that the insurance company should have clarified the exclusions more prominently at the time of issuing the policy.

- They also invoked the ‘contra proferentem rule,’ which states that any ambiguity in an insurance policy must be interpreted in favor of the insured.

Supreme Court’s Ruling

The Supreme Court ruled in favor of United India Insurance, setting aside the NCDRC order and dismissing the claim.

Key Observations by the Supreme Court:

- “Mere perusal of the note appended to clause 4 would go to show that the appellant had made it clear in the proposal form itself that ‘window display of articles at night is not covered.’”

- “The language of clauses 4, 5, and 12 is plain, clear, and unambiguous, and creates no confusion.”

- “If the burglary had been committed during business hours, the stolen items would have been covered. However, since the incident took place at night and the stolen items were kept outside the safe, the claim was justifiably denied.”

- “In contracts of insurance, policyholders must strictly adhere to the terms and conditions, and courts should not rewrite contracts to provide coverage where none exists.”

Legal Precedents Considered

The Supreme Court referred to multiple past judgments on the interpretation of insurance contracts, including:

- General Assurance Society Ltd. v. Chandumull Jain (1966) 3 SCR 500 – Clarified that insurance policies are commercial contracts and must be interpreted strictly.

- United India Insurance Co. Ltd. v. Harchand Rai Chandan Lal (2004) 8 SCC 644 – Reinforced that insurance companies are not liable for claims explicitly excluded in policy terms.

- Oriental Insurance Co. Ltd. v. Sony Cheriyan (1999) 6 SCC 451 – Held that insurance policy exclusions must be enforced as written.

Key Takeaways from the Judgment

- Strict Enforcement of Policy Terms: Courts cannot rewrite insurance contracts to provide coverage beyond the agreed-upon terms.

- Importance of Reading Policy Documents: Policyholders must carefully review exclusions to avoid disputes during claims.

- Limited Role of ‘Contra Proferentem’ Rule: The Court rejected the argument that ambiguous clauses should favor the insured, stating that no ambiguity existed in this case.

- Clear Responsibilities for Policyholders: Businesses should take extra precautions, such as locking valuable stock in safes, to ensure their claims remain valid.

Impact of the Judgment

This ruling reinforces that insurance companies have the right to deny claims that do not adhere to the terms explicitly stated in the policy. It also serves as a warning for businesses to thoroughly understand policy exclusions before purchasing insurance.

Conclusion

The Supreme Court’s judgment in United India Insurance Co. Ltd. v. M/s Orient Treasures Pvt. Ltd. underscores the necessity of strictly interpreting insurance policies. While policyholders expect protection, they must comply with the terms of the policy, especially regarding security requirements. This ruling sets a significant precedent for future insurance disputes, ensuring that claim denials based on clear policy exclusions are legally upheld.

Don’t miss out on the full details! Download the complete judgment in PDF format below and gain valuable insights instantly!

Download Judgment: United India Insuran vs Ms Orient Treasures Supreme Court of India Judgment Dated 13-01-2016.pdf

Direct Downlaod Judgment: Direct downlaod this Judgment

See all petitions in Commercial Insurance Disputes

See all petitions in Other Insurance Cases

See all petitions in Insurance Settlements

See all petitions in Judgment by J. Chelameswar

See all petitions in Judgment by Abhay Manohar Sapre

See all petitions in allowed

See all petitions in supreme court of India judgments January 2016

See all petitions in 2016 judgments

See all posts in Insurance Cases Category

See all allowed petitions in Insurance Cases Category

See all Dismissed petitions in Insurance Cases Category

See all partially allowed petitions in Insurance Cases Category