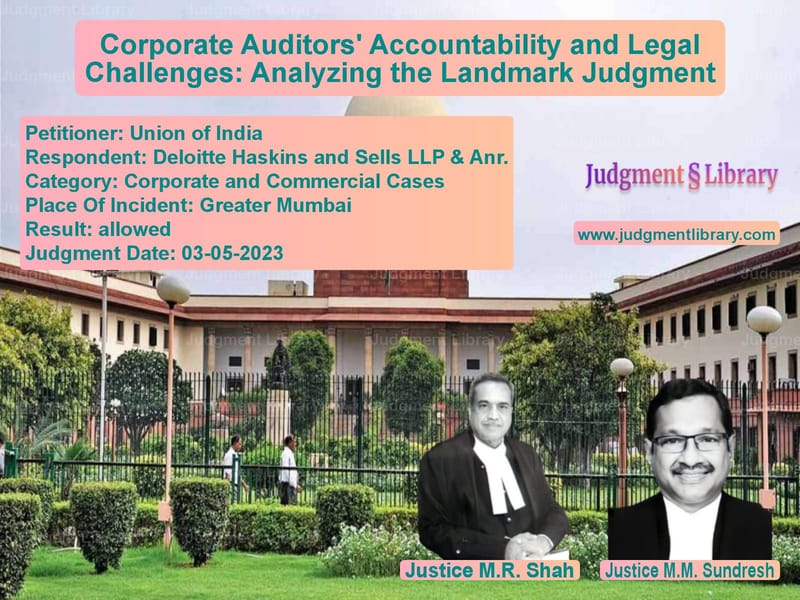

Corporate Auditors’ Accountability and Legal Challenges: Analyzing the Landmark Judgment

The case before the court involved a crucial examination of corporate auditors’ accountability and the legal mechanisms to address fraud perpetrated or abetted by them. The appeals raised significant questions regarding the interpretation of Section 140(5) of the Companies Act, 2013, and the validity of proceedings initiated against auditors even after their resignation. The Union of India, through the Ministry of Corporate Affairs, sought action against Deloitte Haskins & Sells LLP and BSR & Associates LLP, along with other respondents, for their role in the IL&FS Financial Services Limited (IFIN) crisis.

The judgment highlighted the gravity of fraudulent conduct in financial reporting and underscored the necessity of stringent legal provisions to maintain corporate governance. The court emphasized that resignation by an auditor does not absolve them from liability and does not render the proceedings under Section 140(5) infructuous. The provision aims to ensure that auditors found guilty of fraudulent activities face appropriate legal consequences, including debarment from auditing any company for a period of five years.

Petitioner’s Arguments

- The Union of India contended that the auditors played an active role in manipulating financial statements and abetting fraudulent activities within IFIN.

- They argued that Section 140(5) of the Act provides for an independent inquiry by the Tribunal (NCLT) to determine the fraudulent conduct of an auditor, irrespective of their resignation.

- The government emphasized that allowing resignation to terminate proceedings would render the provision ineffective and contrary to its legislative intent.

- They further pointed out that the SFIO report, which was challenged by the respondents, was a conclusive investigation report on IFIN, and not an interim report, as claimed by the auditors.

Respondents’ Arguments

- The respondents, including Deloitte and BSR, argued that once an auditor resigns, the purpose of Section 140(5) is fulfilled, as the primary objective is to change the auditor.

- They contended that the second proviso to Section 140(5), which mandates a five-year debarment, is excessive and should not apply automatically.

- The auditors challenged the validity of the sanction under Section 212(14), arguing that it was issued in undue haste without proper application of mind.

- They further asserted that alternative provisions under the Companies Act, including Sections 241(3) and 447, provided adequate remedies without resorting to Section 140(5).

Court’s Observations

- The court upheld the validity of Section 140(5), stating that it serves a critical purpose in ensuring corporate accountability and financial transparency.

- It ruled that an auditor’s resignation does not nullify proceedings initiated under the provision, as the determination of fraud is a separate and necessary process.

- The court clarified that the second proviso, which imposes a five-year debarment, is a substantive provision and cannot be circumvented through resignation.

- On the issue of the SFIO report, the court rejected the claim that it was an interim report and held that the findings against the auditors were sufficient to warrant prosecution.

Final Decision

- The appeals filed by the Union of India were allowed, and the High Court’s decision to quash the Section 140(5) proceedings was overturned.

- The court reinstated the criminal proceedings and directed the NCLT to continue its inquiry under Section 140(5).

- It held that the auditors found guilty under Section 140(5) would be disqualified from acting as auditors for any company for a period of five years.

- The challenge to the constitutional validity of Section 140(5) was rejected, affirming that it does not violate fundamental rights under Articles 14 and 19(1)(g) of the Constitution.

The judgment reinforces the principle that corporate auditors must be held accountable for their role in financial frauds and cannot escape liability by resigning. It sets a precedent for strict enforcement of corporate governance norms and upholds the integrity of financial reporting mechanisms in India.

Read also: https://judgmentlibrary.com/supreme-court-quashes-high-court-order-in-sarfaesi-auction-dispute/

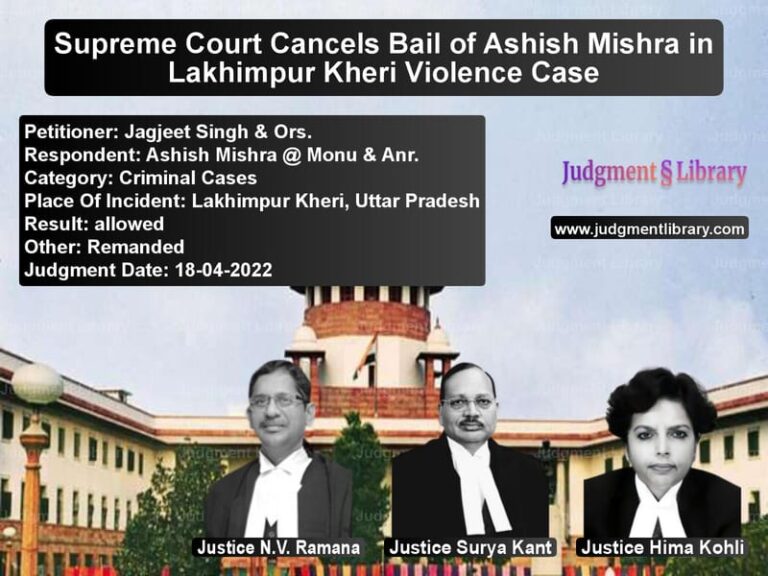

Petitioner Name: Union of India.Respondent Name: Deloitte Haskins and Sells LLP & Anr..Judgment By: Justice M.R. Shah, Justice M.M. Sundresh.Place Of Incident: Greater Mumbai.Judgment Date: 03-05-2023.

Don’t miss out on the full details! Download the complete judgment in PDF format below and gain valuable insights instantly!

Download Judgment: union-of-india-vs-deloitte-haskins-and-supreme-court-of-india-judgment-dated-03-05-2023.pdf

Directly Download Judgment: Directly download this Judgment

See all petitions in Company Law

See all petitions in Corporate Governance

See all petitions in unfair trade practices

See all petitions in Bankruptcy and Insolvency

See all petitions in Shareholder Disputes

See all petitions in Judgment by Mukeshkumar Rasikbhai Shah

See all petitions in Judgment by M.M. Sundresh

See all petitions in allowed

See all petitions in supreme court of India judgments May 2023

See all petitions in 2023 judgments

See all posts in Corporate and Commercial Cases Category

See all allowed petitions in Corporate and Commercial Cases Category

See all Dismissed petitions in Corporate and Commercial Cases Category

See all partially allowed petitions in Corporate and Commercial Cases Category