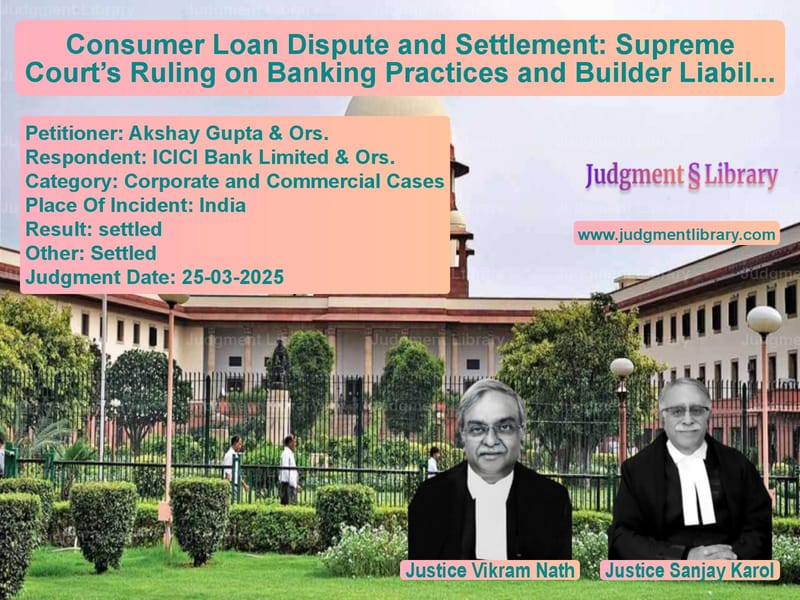

Consumer Loan Dispute and Settlement: Supreme Court’s Ruling on Banking Practices and Builder Liabilities

In a significant ruling, the Supreme Court of India addressed a long-standing dispute involving homebuyers, a real estate builder, and a banking institution. This case revolved around the recall of loans, alleged unfair trade practices, and the legal obligations of both the bank and the builder. The decision holds considerable implications for consumer rights, banking regulations, and financial agreements in India.

Introduction to the Dispute

The petitioners, a group of homebuyers led by Akshay Gupta and others, had approached the National Consumer Dispute Redressal Commission (NCDRC) challenging loan recall notices issued by ICICI Bank Limited. The homebuyers contended that the bank had engaged in unfair trade practices, arguing that it had recalled loans without proper justification and in violation of Reserve Bank of India (RBI) guidelines. However, the NCDRC dismissed their claims, prompting them to appeal to the Supreme Court.

Key Legal Issues Considered

- Whether the recall of loans by ICICI Bank amounted to unfair trade practices under consumer protection laws.

- Whether the homebuyers had the right to challenge the bank’s actions under the Consumer Protection Act, 1986.

- The extent of the builder’s liability in making pre-EMI payments on behalf of homebuyers.

- The legality of the settlement terms proposed during the proceedings.

Arguments Presented Before the Supreme Court

Petitioners’ Arguments (Homebuyers):

- The homebuyers argued that ICICI Bank had arbitrarily recalled their home loans, even though there were ongoing discussions between the bank, the builder, and the borrowers regarding delayed payments.

- They alleged that the bank failed to provide adequate notice before issuing recall notices, violating RBI guidelines.

- They claimed that the builder, Rajsanket Realty Ltd., was also responsible for the financial burden as it had failed to fulfill its commitment of making pre-EMI payments.

The petitioners’ counsel stated: “The bank has acted in an unjust and arbitrary manner. It failed to adhere to regulatory guidelines, unfairly shifting the entire financial burden onto the homebuyers, despite the builder’s contractual obligations to cover pre-EMI payments.”

Respondent’s Arguments (ICICI Bank & Builder):

- ICICI Bank countered that the homebuyers had defaulted on their loan obligations, justifying the recall notices.

- The bank asserted that its actions were in compliance with all contractual agreements and banking regulations.

- The builder argued that its financial obligations were limited and that the homebuyers were contractually bound to fulfill their loan commitments.

The bank’s legal counsel argued: “ICICI Bank has acted in accordance with the agreements signed by the borrowers. The recall of loans was a necessary step, given the continued defaults, and was well within the framework of financial laws.”

Supreme Court’s Analysis and Observations

The Supreme Court examined the contractual obligations of all three parties—the homebuyers, the builder, and the bank. The Court observed:

“This is a classic case where wisdom dawned upon the three parties in a commercial arrangement to settle the dispute amicably, of course, with a little effort by the Court.”

The Court facilitated a structured settlement, outlining the following terms:

- The bank agreed to waive outstanding charges and provide a 30% discount on pre-EMI interest.

- The builder agreed to contribute 50% of the remaining pre-EMI amount.

- The homebuyers agreed to settle the principal loan amount upfront.

In response to the bank’s argument, the Court stated:

“While financial institutions have the right to enforce their agreements, they must do so in a fair and non-arbitrary manner, keeping consumer rights in mind.”

The Court further noted:

“When multiple parties are involved in a financial arrangement, their obligations must be clearly defined, and no single party should bear an undue financial burden.”

Final Judgment and Directions

The Supreme Court allowed the appeals to be disposed of based on the agreed settlement terms. The following directions were issued:

- The bank must issue a ‘No Objection Certificate’ (NOC) upon full compliance by the homebuyers and the builder.

- The builder must complete pending construction and hand over possession of the apartments by March 31, 2025.

- The homebuyers must make their agreed payments within the stipulated time frame.

The ruling reaffirmed the need for fairness in banking practices while recognizing consumer protection as a crucial element in financial agreements.

Petitioner Name: Akshay Gupta & Ors..Respondent Name: ICICI Bank Limited & Ors..Judgment By: Justice Vikram Nath, Justice Sanjay Karol.Place Of Incident: India.Judgment Date: 25-03-2025.

Don’t miss out on the full details! Download the complete judgment in PDF format below and gain valuable insights instantly!

Download Judgment: akshay-gupta-&-ors.-vs-icici-bank-limited-&-supreme-court-of-india-judgment-dated-25-03-2025.pdf

Directly Download Judgment: Directly download this Judgment

See all petitions in Bankruptcy and Insolvency

See all petitions in Corporate Compliance

See all petitions in unfair trade practices

See all petitions in Judgment by Vikram Nath

See all petitions in Judgment by Sanjay Karol

See all petitions in settled

See all petitions in settled

See all petitions in supreme court of India judgments March 2025

See all petitions in 2025 judgments

See all posts in Corporate and Commercial Cases Category

See all allowed petitions in Corporate and Commercial Cases Category

See all Dismissed petitions in Corporate and Commercial Cases Category

See all partially allowed petitions in Corporate and Commercial Cases Category