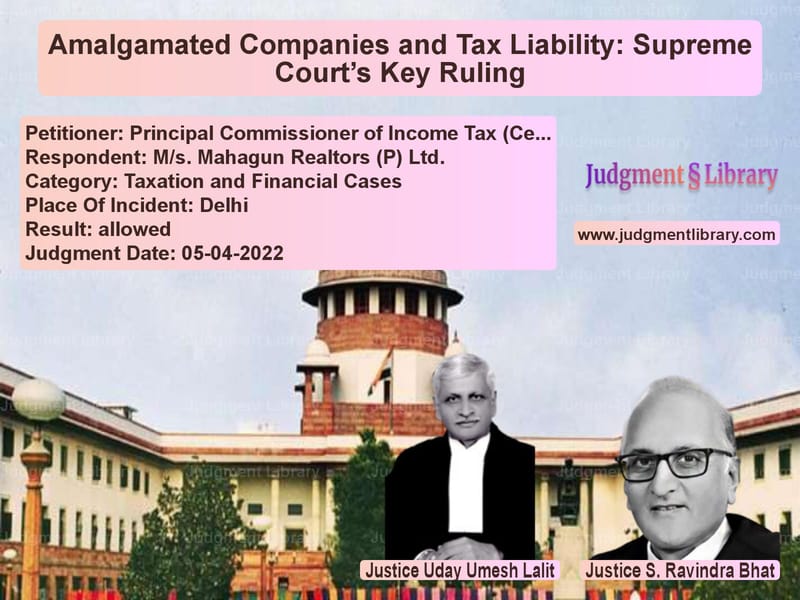

Amalgamated Companies and Tax Liability: Supreme Court’s Key Ruling

The legal battle between the Principal Commissioner of Income Tax (Central) and M/s. Mahagun Realtors (P) Ltd. brought to light critical questions on the taxability of amalgamated entities. The core issue before the Supreme Court was whether an assessment order issued in the name of a non-existent company due to amalgamation was legally valid.

Background of the Case

M/s. Mahagun Realtors Private Limited (MRPL), engaged in real estate development, merged with Mahagun India Private Limited (MIPL) under a High Court order dated 10.09.2007, effective from 01.04.2006. The dispute began when survey and search operations were conducted in the Mahagun Group, uncovering discrepancies in MRPL’s financial records. A notice under Section 153A of the Income Tax Act was issued, followed by assessment proceedings.

The revenue authorities passed an assessment order against MRPL, even though the company had ceased to exist after its merger. The ITAT quashed the order, citing the Supreme Court’s precedent in Principal Commissioner of Income Tax v. Maruti Suzuki India Limited, where assessments against non-existent companies were deemed invalid. The Delhi High Court upheld ITAT’s decision, leading to an appeal by the revenue before the Supreme Court.

Arguments by the Parties

Revenue’s Arguments

- The revenue contended that since both MRPL and MIPL were mentioned in the assessment order, any defect in naming could be cured under Section 292B of the Income Tax Act.

- It argued that the amalgamating company (MRPL) was represented by the amalgamated company (MIPL), and no prejudice was caused by the assessment order.

- The revenue differentiated this case from Maruti Suzuki, where the final assessment order did not mention the amalgamated company at all.

- It was also claimed that at the time of search operations, MRPL had filed returns in its own name, making the assessment valid.

Respondent’s Arguments

- The respondent asserted that after its merger, MRPL ceased to exist, making the assessment against it a legal nullity.

- It cited the Supreme Court’s ruling in Saraswati Industrial Syndicate v. Commissioner of Income Tax, which held that an amalgamated company loses its independent existence.

- The respondent maintained that proceedings initiated against a non-existent entity were void ab initio.

- It relied on Spice Infotainment Ltd v. CIT, where assessments made in the name of dissolved companies were struck down.

Supreme Court’s Judgment

The Supreme Court overturned the High Court’s ruling and restored the revenue’s appeal before ITAT for reconsideration on merits.

Key Findings of the Court

- The Court acknowledged that MRPL ceased to exist post-amalgamation but held that its business continued under MIPL.

- Unlike Maruti Suzuki, the assessment order in this case mentioned both the amalgamating and amalgamated companies, making it a procedural defect rather than a jurisdictional error.

- The Court noted that MRPL had actively participated in assessment proceedings, contradicting its argument that it was non-existent.

- The Court held that whether corporate death of an entity invalidates an assessment order depends on the terms of amalgamation and case-specific facts.

The Court reasoned:

“In the facts of this case, the conduct of the assessee, commencing from the date the search took place, and before all forums, reflects that it consistently held itself out as the assessee.”

Impact of the Judgment

This ruling clarifies that in tax matters involving amalgamated companies:

- The legal identity of the amalgamating company ceases, but tax liabilities may still be enforceable against the amalgamated entity.

- Active participation in proceedings can override technical objections based on nomenclature.

- Section 292B can cure procedural defects in assessment orders if substantive tax liability is unaffected.

- Assessment orders must clearly reflect the successor company’s liability to avoid litigation.

Conclusion

The Supreme Court’s ruling provides much-needed clarity on tax assessments of amalgamated entities. It ensures that companies cannot escape tax liability merely by merging into another entity while also safeguarding against arbitrary assessments against dissolved firms. This case reinforces the need for clear documentation and timely disclosures in corporate tax matters.

Read also: https://judgmentlibrary.com/supreme-court-clears-tax-official-of-misconduct-in-flipkart-vat-dispute/

Petitioner Name: Principal Commissioner of Income Tax (Central) – 2.Respondent Name: M/s. Mahagun Realtors (P) Ltd..Judgment By: Justice Uday Umesh Lalit, Justice S. Ravindra Bhat.Place Of Incident: Delhi.Judgment Date: 05-04-2022.

Don’t miss out on the full details! Download the complete judgment in PDF format below and gain valuable insights instantly!

Download Judgment: principal-commission-vs-ms.-mahagun-realtor-supreme-court-of-india-judgment-dated-05-04-2022.pdf

Directly Download Judgment: Directly download this Judgment

See all petitions in Income Tax Disputes

See all petitions in Tax Evasion Cases

See all petitions in Banking Regulations

See all petitions in Judgment by Uday Umesh Lalit

See all petitions in Judgment by S Ravindra Bhat

See all petitions in allowed

See all petitions in supreme court of India judgments April 2022

See all petitions in 2022 judgments

See all posts in Taxation and Financial Cases Category

See all allowed petitions in Taxation and Financial Cases Category

See all Dismissed petitions in Taxation and Financial Cases Category

See all partially allowed petitions in Taxation and Financial Cases Category