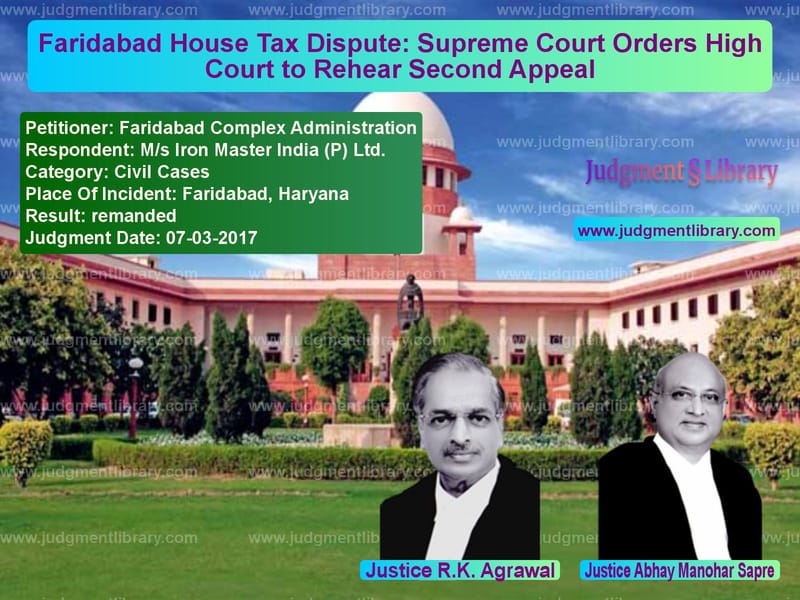

Faridabad House Tax Dispute: Supreme Court Orders High Court to Rehear Second Appeal

The case of Faridabad Complex Administration vs. M/s Iron Master India (P) Ltd. is a significant ruling by the Supreme Court of India concerning municipal taxation and judicial review of second appeals. This case revolves around the collection of House Tax imposed by the Faridabad municipal authorities and the procedural lapses in handling taxpayer objections. The Supreme Court ruled that the High Court had wrongly dismissed the second appeal without framing substantial questions of law and ordered a fresh hearing.

Background of the Case

The appellant, Faridabad Complex Administration, is a municipal corporation responsible for collecting various taxes under the Haryana Municipal Act, 1973. The respondent, M/s Iron Master India (P) Ltd., a company based in Faridabad, was subjected to house tax assessments for the years 1991-92, 1992-93, and 1993-94. The company challenged the tax demand notice dated November 20, 1993, amounting to Rs. 48,599.40, arguing that it was illegal and violated due process.

The company filed a civil suit seeking a permanent injunction against the municipal authorities from recovering the tax. It also sought a declaration that the demand notice was illegal. The trial court dismissed the suit, ruling in favor of the municipality. However, the appellate court reversed this decision, leading the municipality to file a second appeal in the Punjab and Haryana High Court. The High Court dismissed the second appeal at the preliminary stage, stating that no substantial question of law arose. The matter was then brought before the Supreme Court.

Legal Issues Before the Supreme Court

- Was the High Court justified in dismissing the second appeal without framing substantial questions of law?

- Did the municipal corporation violate procedural requirements under the Haryana Municipal Act while imposing the house tax?

- Did the taxpayer have an alternative remedy under the Act, and was the civil suit maintainable?

- Was the jurisdiction of civil courts barred in municipal tax matters?

Arguments by the Petitioner (Faridabad Complex Administration)

The municipal corporation presented the following arguments:

- The High Court had erred in dismissing the second appeal without examining key legal issues.

- The company had alternative statutory remedies under the Haryana Municipal Act, making the civil suit non-maintainable.

- The tax assessment was conducted legally, and the respondent had failed to follow the proper procedure for objections.

- The appellate court had wrongly overturned the trial court’s decision without sufficient legal justification.

Arguments by the Respondent (M/s Iron Master India Pvt. Ltd.)

The taxpayer countered with the following arguments:

- The tax demand was illegal because the municipality had failed to decide on the objections before finalizing the assessment.

- The company had duly filed objections and sought a personal hearing, which the municipal authorities ignored.

- The municipal corporation failed to provide documentary evidence proving that proper procedures were followed.

- The civil court had jurisdiction to entertain the suit as the taxpayer’s fundamental right to due process had been violated.

Supreme Court’s Observations

The Supreme Court examined the dismissal of the second appeal by the Punjab and Haryana High Court and ruled that the dismissal was incorrect. The Court stated:

“The appeal did involve substantial questions of law and, therefore, the High Court should have admitted the appeal by first framing proper substantial questions of law arising in the case.”

The Court further observed:

- The case involved key legal questions related to tax assessment procedures, alternative remedies, and civil court jurisdiction.

- The High Court had a duty to frame substantial questions of law before dismissing the appeal.

- The appellate court’s ruling in favor of the taxpayer raised important legal issues that needed to be examined in detail.

- The failure to decide taxpayer objections before imposing tax demanded judicial scrutiny.

Final Judgment

On March 7, 2017, the Supreme Court ruled:

- The appeal by the municipal corporation was allowed.

- The High Court’s decision dismissing the second appeal was set aside.

- The case was remanded to the Punjab and Haryana High Court for fresh hearing.

- The High Court was directed to admit the second appeal, frame appropriate substantial questions of law, and decide the case on merits.

- The High Court was asked to issue notice to the municipal authorities and expedite the hearing.

Legal Implications of the Judgment

This ruling has several important implications for taxation and judicial review:

- High Court’s Role in Second Appeals: The judgment clarifies that High Courts must frame substantial questions of law before dismissing second appeals under Section 100 of the Code of Civil Procedure.

- Municipal Taxation Procedures: Local authorities must follow due process, including resolving taxpayer objections before issuing tax demands.

- Jurisdiction of Civil Courts: The ruling affirms that civil courts have jurisdiction in tax matters where procedural violations occur.

- Alternative Remedies in Tax Cases: Taxpayers must be aware of statutory remedies available under municipal laws before approaching civil courts.

Impact on Future Tax Disputes

This judgment sets a critical precedent for handling municipal tax disputes:

- Municipalities must ensure that assessment procedures comply with statutory requirements.

- Taxpayers have the right to challenge tax assessments if due process is not followed.

- High Courts must exercise due diligence in admitting and hearing second appeals involving tax disputes.

Conclusion

The Supreme Court’s decision in Faridabad Complex Administration vs. M/s Iron Master India (P) Ltd. reinforces the importance of procedural fairness in tax assessments. It upholds the principle that taxpayers must be given a fair opportunity to challenge tax demands and that courts must exercise their appellate jurisdiction responsibly. By remanding the case to the High Court, the ruling ensures that key legal issues are properly examined, setting a valuable precedent for future municipal tax disputes.

Don’t miss out on the full details! Download the complete judgment in PDF format below and gain valuable insights instantly!

Download Judgment: Faridabad Complex Ad vs Ms Iron Master Indi Supreme Court of India Judgment Dated 07-03-2017.pdf

Direct Downlaod Judgment: Direct downlaod this Judgment

See all petitions in Property Disputes

See all petitions in Debt Recovery

See all petitions in Damages and Compensation

See all petitions in Judgment by R K Agrawal

See all petitions in Judgment by Abhay Manohar Sapre

See all petitions in Remanded

See all petitions in supreme court of India judgments March 2017

See all petitions in 2017 judgments

See all posts in Civil Cases Category

See all allowed petitions in Civil Cases Category

See all Dismissed petitions in Civil Cases Category

See all partially allowed petitions in Civil Cases Category