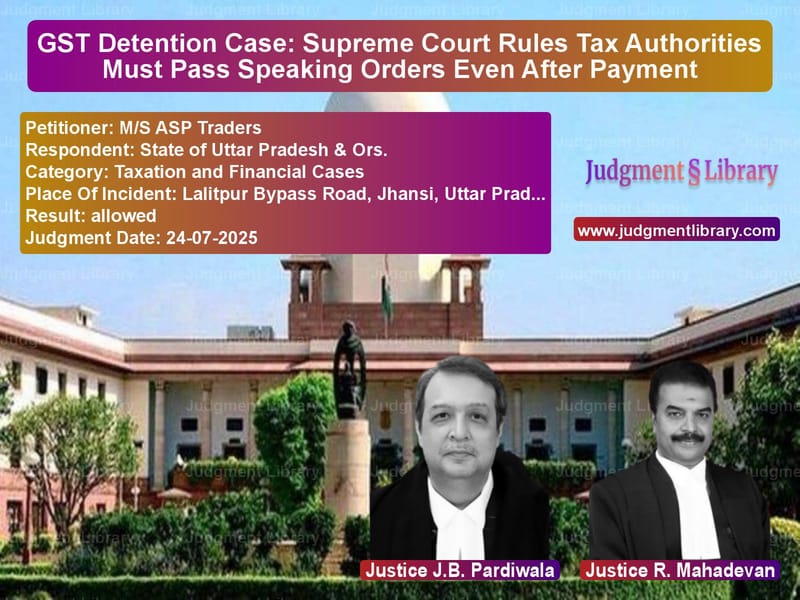

GST Detention Case: Supreme Court Rules Tax Authorities Must Pass Speaking Orders Even After Payment

In a significant ruling that reinforces taxpayer rights and procedural fairness under the Goods and Services Tax (GST) regime, the Supreme Court of India has delivered a judgment ensuring that tax authorities cannot avoid their statutory obligation to pass reasoned orders even when taxpayers make payments to secure release of detained goods. The case involved M/s ASP Traders, a registered dealer in red arecanut from Karnataka, whose goods were detained during transit by the Uttar Pradesh GST authorities.

The dispute began on January 17, 2022, when a vehicle transporting 17,850 kg of dry arecanut valued at approximately Rs. 51.72 lakh was intercepted by the Mobile Squad at Lalitpur Bypass Road in Jhansi. During inspection, the authorities found that 7 bags were missing from the original consignment and alleged that the consignee, M/s Diamond Trading Company, was non-existent. The goods were detained, and a notice was issued under Section 129(3) of the CGST Act demanding payment of tax and penalty.

The appellant submitted a detailed reply denying all allegations but, due to pressing business exigencies, deposited Rs. 7,20,440 towards IGST through Form GST DRC-03 on January 27, 2022. The goods were subsequently released. However, despite repeated requests, the tax authorities refused to pass a final order under Section 129(3), claiming that the proceedings stood concluded upon payment under Section 129(5) of the CGST Act.

The appellant approached the High Court seeking directions to the authorities to pass a speaking order, but the High Court dismissed the writ petition, observing that “once the proceedings in respect of notice under Section 129(3) of the Act stood concluded in terms of Section 129(5) of the Act read with Rule 142(3) of the Rules, no mandamus can be issued to the respondent no. 3 to pass an order under Section 129(3) of the CGST/UPGST/IGST Act.”

Before the Supreme Court, the appellant’s counsel, Mr. Pawanshree Agrawal, argued that “it is a settled position in law that every show cause notice must culminate in a reasoned final order. Such an order is essential to enable the person affected to avail all statutory remedies.” He emphasized that “the payment of penalty cannot be treated as voluntarily under Form GST DRC-03, as no show cause notice or statement in Form GST DRC-01 was ever issued by the respondent authorities requiring the appellant to make such a deposit.”

The appellant further contended that “even if it is assumed that the penalty was paid voluntarily to secure release of the goods, Respondent No.3 was still under a statutory obligation to pass an order in Form GST MOV-09, in accordance with Section 129(3) of the CGST Act, 2017.” The counsel stressed that “an order must be passed under Section 129(3) even if the penalty amount is paid during the pendency of proceedings, so as to preserve the taxpayer’s right of appeal under section 107 of the CGST Act, 2017.”

On the other side, the respondents, represented by Mr. Bhakti Vardhan Singh, argued that “although Section 129(3) requires a notice followed by an order, Section 129(5) clearly stipulates that upon payment of the amount under Section 129(1), ‘all proceedings in respect of the notice specified in sub-section (3) shall be deemed to be concluded’ and thus, no further order is necessary.” They maintained that “Rule 142(3) of the CGST Rules reinforces this position stating that if payment is made after issuance of the notice under Section 129(3) but before passing of the order, the proceedings shall stand concluded.”

The Supreme Court, in its judgment delivered by Justices J.B. Pardiwala and R. Mahadevan, carefully analyzed the statutory provisions and the binding CBIC Circular dated April 13, 2018. The Court made several crucial observations that have far-reaching implications for GST proceedings across the country.

The Court held that “every show cause notice must culminate in a final, reasoned order. While Section 129(5) of the CGST Act, 2017 provides that proceedings shall be deemed to be concluded upon payment of tax and penalty, this deeming fiction cannot be interpreted to imply that the assessee has agreed to waive or abandon the right to challenge the levy.” The judges emphasized that “the term ‘conclusion’ as used in Section 129(5) merely signifies that no further proceedings for prosecution will be initiated. It does not absolve the responsibility of the proper officer to pass an order concluding the proceedings.”

Addressing the specific circumstances of the case, the Court noted that “the language of section 129(3) is categorical in stating that the officer ‘shall issue a notice… and thereafter, pass an order’. The use of the words ‘and thereafter’ reinforces the mandatory nature of passing a reasoned order, regardless of payment, particularly where protest or dispute is raised.”

The Court made a significant observation about the limitations of the GST payment portal, noting that “the GST payment portal permits payments only through Form GST DRC-03, which is automatically classified as a voluntary payment, and does not provide any mechanism for an assessee to indicate that the payment is being made under protest. In the absence of such an option, payments made under commercial compulsion or business necessity – such as for securing release of detained goods – may be erroneously construed as voluntary, resulting in undue prejudice.”

In a powerful statement about constitutional principles, the Court declared that “the payment by an assessee will not absolve the responsibility of the proper officer to pass an order justifying the demand of tax and penalty. The assessee, even by election, cannot be treated to have waived his right against the illegality committed by the proper officer or acquiesced to the demand, as by the constitutional mandate under Article 265 of the Constitution, no tax can be levied or collected except with the authority of law.”

The Court drew support from its earlier decision in M/s Kranti Associates (P) Ltd & Anr. v. Masood Ahmed Khan & Ors., emphasizing that “fairness, transparency, and accountability are inseparable from the duty to provide reasons. The Court held that failure to furnish reasons violates the principles of natural justice and renders the right of appeal or judicial review illusory.”

The Supreme Court specifically outlined the importance of reasoned orders, noting that “insistence on recording of reasons is meant to serve the wider principle of justice that justice must not only be done it must also appear to be done as well” and that “reasons facilitate the process of judicial review by superior Courts.”

In its final ruling, the Court set aside the High Court’s order and directed that “Respondent No.3 is directed to pass a reasoned final order under section 129(3) of the CGST Act, 2017, in Form GST MOV-09, after granting an opportunity of being heard as mandated under Section 129(4), and upload the summary thereof in Form GST DRC-07 within a period of one month from the date of receipt of a copy of this judgment.”

This judgment represents a significant victory for taxpayer rights and procedural fairness in the GST regime. It ensures that even when businesses make payments under commercial compulsion to secure release of detained goods, they retain their right to challenge the legality of the demand through proper appellate channels. The ruling reinforces that tax authorities cannot use technical provisions to avoid their fundamental obligation to pass reasoned orders that can be subjected to judicial scrutiny.

The Supreme Court’s decision serves as an important reminder that procedural safeguards and principles of natural justice are not mere technicalities but essential components of a fair tax administration system. By ensuring that taxpayers have access to proper adjudication and appellate remedies, the judgment strengthens the foundations of the GST regime and promotes confidence in India’s tax administration system.

Petitioner Name: M/S ASP Traders.Respondent Name: State of Uttar Pradesh & Ors..Judgment By: Justice J.B. Pardiwala, Justice R. Mahadevan.Place Of Incident: Lalitpur Bypass Road, Jhansi, Uttar Pradesh.Judgment Date: 24-07-2025.Result: allowed.

Don’t miss out on the full details! Download the complete judgment in PDF format below and gain valuable insights instantly!

Download Judgment: ms-asp-traders-vs-state-of-uttar-prade-supreme-court-of-india-judgment-dated-24-07-2025.pdf

Directly Download Judgment: Directly download this Judgment

See all petitions in GST Law

See all petitions in Tax Refund Disputes

See all petitions in Customs and Excise

See all petitions in Judgment by J.B. Pardiwala

See all petitions in Judgment by R. Mahadevan

See all petitions in allowed

See all petitions in supreme court of India judgments July 2025

See all petitions in 2025 judgments

See all posts in Taxation and Financial Cases Category

See all allowed petitions in Taxation and Financial Cases Category

See all Dismissed petitions in Taxation and Financial Cases Category

See all partially allowed petitions in Taxation and Financial Cases Category