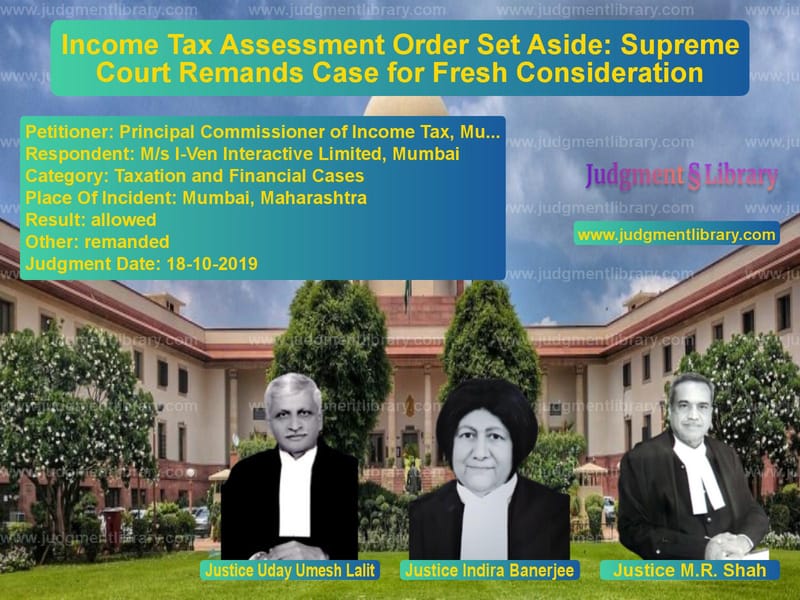

Income Tax Assessment Order Set Aside: Supreme Court Remands Case for Fresh Consideration

The case of Principal Commissioner of Income Tax, Mumbai vs. M/s I-Ven Interactive Limited, Mumbai revolves around a dispute concerning the validity of an income tax assessment order under Section 143(3) of the Income Tax Act, 1961. The Supreme Court, in its judgment dated October 18, 2019, set aside the orders of the High Court, Income Tax Appellate Tribunal (ITAT), and Commissioner of Income Tax (CIT-Appeals), and remanded the matter for reconsideration on merits.

Background of the Case

Filing of Income Tax Return

The respondent-assessee, M/s I-Ven Interactive Limited, filed its income tax return for Assessment Year 2006-07 on November 28, 2006, declaring a total income of Rs. 3,38,71,716. The return was filed electronically and later accompanied by a hard copy submission on December 5, 2006.

Assessment Proceedings

The Income Tax Department processed the return under Section 143(1) of the Income Tax Act. A notice under Section 143(2) was issued on October 5, 2007, at the address available in the PAN database. Additional notices under Section 143(2) and Section 142(1) were issued on multiple occasions in 2008, along with questionnaires requesting additional details from the assessee. The company’s representatives appeared before the Assessing Officer on November 28, 2008, and December 4, 2008.

Challenging the Notices

The assessee challenged the validity of the notices, arguing that:

- The notices were not served at the correct address since the company had shifted to a new location.

- The subsequent notices received by the company were beyond the limitation period prescribed under Section 143(2).

- The assessment order, completed on December 24, 2008, was invalid due to lack of proper service of notice.

Assessment Order

The Assessing Officer proceeded with the assessment under Section 143(3), making a disallowance of Rs. 8,91,17,643 under Section 14A and computing the total taxable income as Rs. 5,52,45,930.

Legal Proceedings

Order of the Commissioner of Income Tax (Appeals)

- The CIT (Appeals) allowed the assessee’s appeal, holding that the Assessing Officer did not assume valid jurisdiction under Section 143(2).

- The CIT (Appeals) found that no notice had been served within the prescribed time at the assessee’s new address.

- The assessment order was deemed invalid due to non-service of notice within the limitation period.

Income Tax Appellate Tribunal (ITAT) Decision

The Revenue challenged the CIT(A) decision before the ITAT, which dismissed the appeal. The ITAT upheld the CIT(A)’s findings that the assessment order was invalid.

Bombay High Court Decision

- The Revenue filed an appeal before the Bombay High Court.

- The High Court upheld the ITAT’s ruling, affirming that the assessment order was legally unsustainable due to improper service of notice.

- The High Court held that mere mentioning of a new address in the income tax return was sufficient to discharge the company’s responsibility.

Supreme Court’s Observations

Arguments by the Revenue

- The Assessing Officer sent notices to the address available in the PAN database, as no intimation of a change of address was received.

- There was no evidence to prove that the company informed the department about the new address.

- The assessee’s challenge to the service of notice was merely technical and should not invalidate the assessment order.

Arguments by the Assessee

- The company had officially changed its address and the Assessing Officer was aware of it.

- The subsequent service of notice, which was beyond the limitation period, rendered the assessment invalid.

- The High Court rightly held that mentioning the new address in the return was sufficient notice to the tax authorities.

Supreme Court’s Findings

- The Assessing Officer was justified in issuing the notice to the address available in the PAN database.

- The assessee failed to produce any evidence showing that it had formally intimated the Assessing Officer about the new address.

- The filing of Form 18 with the Registrar of Companies was not sufficient to notify the Income Tax Department of the address change.

- The Assessing Officer complied with the requirement of issuing a notice under Section 143(2) within the prescribed period.

Setting Aside Previous Orders

- The Supreme Court set aside the orders of the CIT (Appeals), ITAT, and the Bombay High Court.

- The case was remanded to the CIT (Appeals) to consider the appeal on merits rather than dismissing it on procedural grounds.

Key Takeaways from the Judgment

- Service of Notice and PAN Address: The Supreme Court clarified that unless formally updated, the PAN database address remains the valid address for service of notices.

- Filing of Form 18 is Insufficient: Companies must explicitly inform the tax authorities of any change in address to ensure proper service of notices.

- Assessment Orders Cannot Be Set Aside on Mere Technicalities: The Supreme Court reinforced that procedural lapses should not lead to an automatic quashing of assessment orders.

- Remand for Merits-Based Consideration: The judgment ensures that tax disputes are decided on substantive grounds rather than dismissed due to technical objections.

Conclusion

This Supreme Court ruling highlights the importance of procedural compliance by both taxpayers and tax authorities. While taxpayers must ensure proper communication of address changes, tax authorities must exercise diligence in serving notices. By remanding the matter for a decision on merits, the judgment reinforces the principle that procedural lapses should not obstruct the determination of tax liability.

Petitioner Name: Principal Commissioner of Income Tax, Mumbai.Respondent Name: M/s I-Ven Interactive Limited, Mumbai.Judgment By: Justice Uday Umesh Lalit, Justice Indira Banerjee, Justice M.R. Shah.Place Of Incident: Mumbai, Maharashtra.Judgment Date: 18-10-2019.

Don’t miss out on the full details! Download the complete judgment in PDF format below and gain valuable insights instantly!

Download Judgment: Principal Commission vs Ms I-Ven Interactiv Supreme Court of India Judgment Dated 18-10-2019.pdf

Direct Downlaod Judgment: Direct downlaod this Judgment

See all petitions in Income Tax Disputes

See all petitions in Tax Evasion Cases

See all petitions in Banking Regulations

See all petitions in Corporate Compliance

See all petitions in Judgment by Uday Umesh Lalit

See all petitions in Judgment by Indira Banerjee

See all petitions in Judgment by Mukeshkumar Rasikbhai Shah

See all petitions in allowed

See all petitions in Remanded

See all petitions in supreme court of India judgments October 2019

See all petitions in 2019 judgments

See all posts in Taxation and Financial Cases Category

See all allowed petitions in Taxation and Financial Cases Category

See all Dismissed petitions in Taxation and Financial Cases Category

See all partially allowed petitions in Taxation and Financial Cases Category